(Updated on 14 March to correct proportion in headline).

More than three-quarters (76%) of Europe’s office buildings are at risk of obsolescence by the end of this decade unless landlords invest in improvements or find alternative uses, Cushman & Wakefield has warned in a wide-ranging report published at the Mipim conference in Cannes.

The report finds the combination of changing work patterns, occupier demand, increasing legislative action from European governments around minimum sustainability standards, and an uncertain economic backdrop is behind the stark risk to office assets.

Landlords are being urged to act now to mitigate the impact of sustainability regulations from governments on their portfolios. Offices below a certain level of energy performance are under threat of legal obsolescence. In the UK, for example, commercial buildings must have a minimum energy performance rating of E by April 2023, increasing to B by 2030.

Across Europe, hybrid working patterns have also led office occupiers to seek out higher quality workplaces meeting the latest environmental, wellbeing and digital connectivity standards, Cushman says. This top-quality space accounted for over half (54%) of total European office demand between 2019-22. This trend is expected to intensify as demand exceeds supply in many markets including Prague, Budapest, Milan, Warsaw, Madrid, Barcelona and London.

But around half of Europe’s existing office stock is over 30 years old and only 14% has been built or substantially modernised in the last 10 years years.

Cushman & Wakefield’s analysis estimates that current office stock can be split as:

- Top: around 24%, built in the last decade, fits modern office usage and is in high demand.

- Middle: a large proportion of 62% requires repositioning to avoid deterioration.

- Bottom: 14%, ageing, non-updated stock that is in many ways already obsolete.

James Young, head of investor services EMEA & APAC, Cushman & Wakefield, said in a statement: “The office sector is facing a critical chapter of necessary adaptation, evolution, and recalibration. Across Europe there is strong demand for offices, but occupiers drive the market and they are increasingly focused on the very best workplaces.

“For owners of older, lower quality assets, doing nothing is not a strategy. Landlords that reinvest in sustainability credentials, amenities, sense of place and community engagement to move their assets into top quality ratings will benefit from this flight to quality. Those that do not will face diminishing returns.”

The report predicts a growing imbalance between available top-grade space and and stock that could be obsolete or has the potential to be so unless immediate action is taken.

Cushman says there are many solutions that can address the sustainability requirements and tenant needs. These include repositioning the asset to upgrade its amenities and sustainability, and through community-oriented offerings and events. It can also be to repurpose all or some of the office for other uses, such as residential, industrial, life sciences or healthcare.

Young added: “There is much to be gained even by those facing the stiffest of headwinds. Addressing the challenge head-on with a proactive, creative, and strategic approach will help owners and investors recover value and generate returns. It is important when doing so to assess each office individually, as well as in the context of broader portfolios. There is no ‘one size fits all solution’ but learnings from around the world can allow evolution to take place in a measured and intentional manner.”

The report analysed office stock by age and grade; construction and completions (historically and estimates for future activity); and occupier demand trends and utilisation since the pandemic. This was then combined with labour market projections to assess aggregate supply and demand in the European office sector, featuring a select number of major markets. Overall, the report analyses 218 million square metres of office stock in 14 markets in 11 countries across Europe.

article9 Min ReadMarch 16, 2023 10:49 AMLocal leaders discuss investor appetite amid economic headwinds.

article9 Min ReadMarch 16, 2023 10:49 AMLocal leaders discuss investor appetite amid economic headwinds. article1 Min ReadMarch 16, 2023 07:06 AMCoStar News and sister publication Business Immo team up to quiz the leader of the region around Paris.

article1 Min ReadMarch 16, 2023 07:06 AMCoStar News and sister publication Business Immo team up to quiz the leader of the region around Paris.

article2 Min ReadMarch 16, 2023 06:20 AMParters commit to Joint Venture To Improve Birmingham's Knowledge Quarter

article2 Min ReadMarch 16, 2023 06:20 AMParters commit to Joint Venture To Improve Birmingham's Knowledge Quarter article1 Min ReadMarch 16, 2023 05:49 AMThe IWG chief executive says commuting is 'one of the craziest inventions of the last 100 years' and on the ropes anywhere it is long, inefficient and expensive.

article1 Min ReadMarch 16, 2023 05:49 AMThe IWG chief executive says commuting is 'one of the craziest inventions of the last 100 years' and on the ropes anywhere it is long, inefficient and expensive.

article2 Min ReadMarch 16, 2023 05:10 AMMoney is not an issue for the US property owner and developer after Stone Point Capital became involved last month.

article2 Min ReadMarch 16, 2023 05:10 AMMoney is not an issue for the US property owner and developer after Stone Point Capital became involved last month.

article2 Min ReadMarch 15, 2023 06:10 PMGlobal markets were rattled by the big bank's troubles, prompting attendees at the Mipim property conference to ponder the impact on their industry.

article2 Min ReadMarch 15, 2023 06:10 PMGlobal markets were rattled by the big bank's troubles, prompting attendees at the Mipim property conference to ponder the impact on their industry.

article1 Min ReadMarch 15, 2023 10:55 AMYoung is moving from London as group looks to double in size across the region.

article1 Min ReadMarch 15, 2023 10:55 AMYoung is moving from London as group looks to double in size across the region.

article1 Min ReadMarch 15, 2023 08:37 AMJames Porter moves from managing director - occupier solutions.

article1 Min ReadMarch 15, 2023 08:37 AMJames Porter moves from managing director - occupier solutions.

article1 Min ReadMarch 15, 2023 07:07 AMCity centre site is destined for mix of housing units and sits close to railway station.

article1 Min ReadMarch 15, 2023 07:07 AMCity centre site is destined for mix of housing units and sits close to railway station. article2 Min ReadMarch 15, 2023 06:48 AMExperts cite North East's Newcastle Helix scheme as an example of successful city centre regeneration around higher education.

article2 Min ReadMarch 15, 2023 06:48 AMExperts cite North East's Newcastle Helix scheme as an example of successful city centre regeneration around higher education. article1 Min ReadMarch 15, 2023 06:18 AMHorrell also talks to CoStar News about sector opportunities, getting deals done and how the Chancellor could help business growth.

article1 Min ReadMarch 15, 2023 06:18 AMHorrell also talks to CoStar News about sector opportunities, getting deals done and how the Chancellor could help business growth.

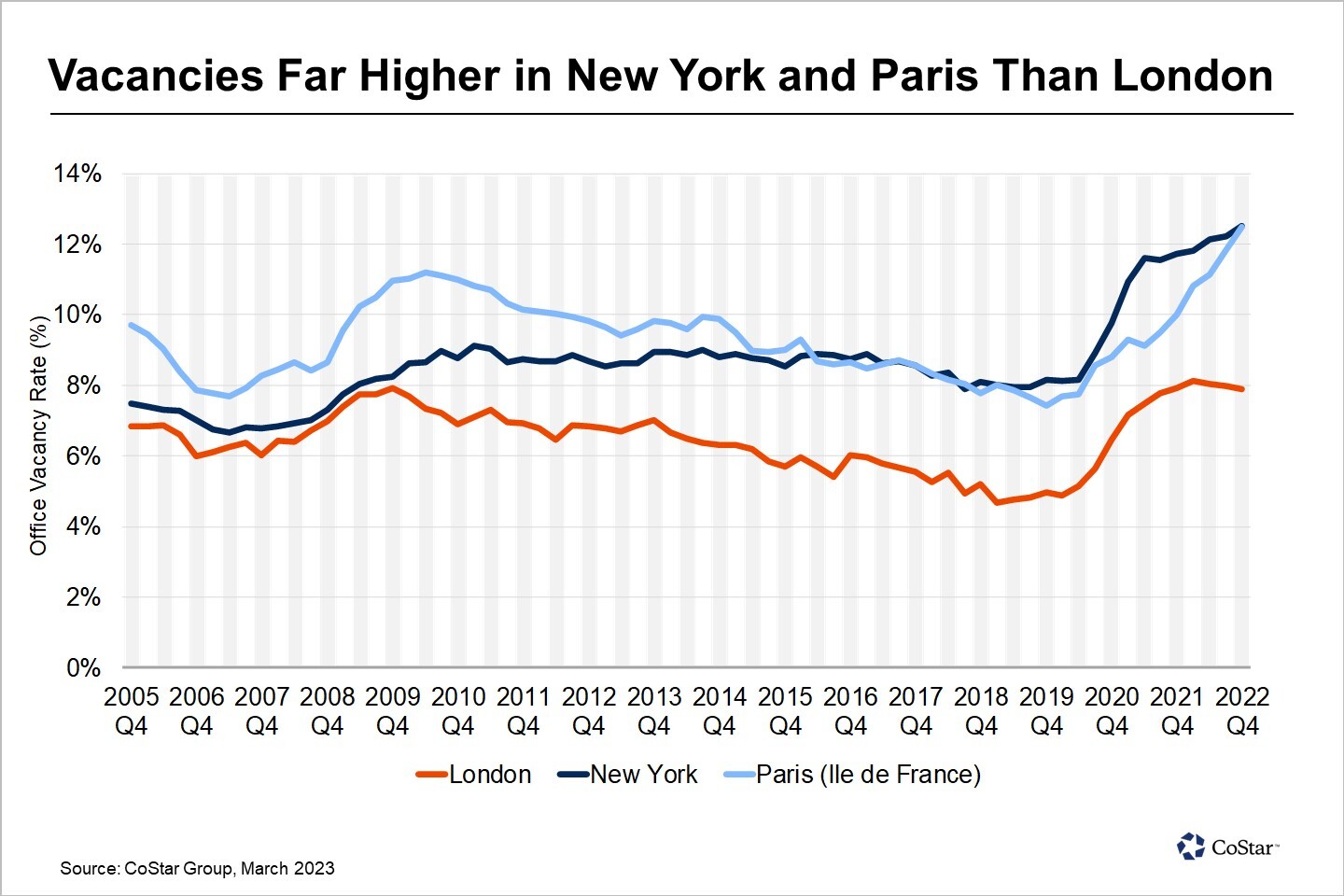

article5 Min ReadMarch 14, 2023 09:36 AMVacancies have stabilised at lower levels in London but yields are rising.

article5 Min ReadMarch 14, 2023 09:36 AMVacancies have stabilised at lower levels in London but yields are rising.

article3 Min ReadMarch 14, 2023 09:21 AMCushman report warns that a combination of factors means landlords must act now.

article3 Min ReadMarch 14, 2023 09:21 AMCushman report warns that a combination of factors means landlords must act now.

article2 Min ReadMarch 14, 2023 07:32 AMDeal includes 64% of stake in Icade Santé and Icade Healthcare Europe's portfolio of assets.

article2 Min ReadMarch 14, 2023 07:32 AMDeal includes 64% of stake in Icade Santé and Icade Healthcare Europe's portfolio of assets.

article1 Min ReadMarch 14, 2023 05:41 AMThe commercial and residential agent is launching a dedicated BTR division at the real estate conference.

article1 Min ReadMarch 14, 2023 05:41 AMThe commercial and residential agent is launching a dedicated BTR division at the real estate conference.

article2 Min ReadMarch 14, 2023 05:02 AMThe duo has teamed up with transport group Ascendal to announce the plans at the Mipim conference.

article2 Min ReadMarch 14, 2023 05:02 AMThe duo has teamed up with transport group Ascendal to announce the plans at the Mipim conference.

article13 Min ReadMarch 13, 2023 10:25 AMCristina Garcia-Peri, senior partner and head of strategy and corporate development at Azora, catches up with CoStar News.

article13 Min ReadMarch 13, 2023 10:25 AMCristina Garcia-Peri, senior partner and head of strategy and corporate development at Azora, catches up with CoStar News.

article1 Min ReadMarch 13, 2023 06:20 AMThe transaction for the Pullman Cannes Mandelieu Royal Casino has completed as the world's biggest real estate conference gets underway in the city.

article1 Min ReadMarch 13, 2023 06:20 AMThe transaction for the Pullman Cannes Mandelieu Royal Casino has completed as the world's biggest real estate conference gets underway in the city.

article2 Min ReadMarch 13, 2023 05:38 AMThe acquisition of a majority stake in Germany's Redos enables it to create a huge retail warehouse park portfolio.

article2 Min ReadMarch 13, 2023 05:38 AMThe acquisition of a majority stake in Germany's Redos enables it to create a huge retail warehouse park portfolio.

article4 Min ReadMarch 12, 2023 07:56 AMThe UK minister for investment, a US economics star and Amanda Staveley to be among speakers as 23,000 prepare to descend on Cannes for the world's largest real estate conference.

article4 Min ReadMarch 12, 2023 07:56 AMThe UK minister for investment, a US economics star and Amanda Staveley to be among speakers as 23,000 prepare to descend on Cannes for the world's largest real estate conference.