Two significant changes will affect the travel and hospitality industry in the U.S. this holiday season.

First, Thanksgiving is a week later, meaning there are five fewer days between Thanksgiving and Christmas and likely more travel compression between the two holidays. Second, Christmas and New Year’s Day move from a Monday last year to a Wednesday this year. Holidays that fall on a Monday are a positive for hotel stays, creating a cherished long weekend. A holiday on a Wednesday, however, does the opposite by suppressing stays.

Like the many ups and downs we have seen in 2024, the upcoming holiday season will be mixed with the Thanksgiving period from Wednesday through Saturday predicted to produce flat to falling occupancy and average daily rate. We expect the former to drop 0.5 percentage points and the latter by 1.2%, resulting in a 2.1% decrease in revenue per available room compared with the same Thanksgiving period a year ago. Average occupancy during the period is projected at 53.1%.

This year’s holiday season between Thanksgiving and Christmas is only 26 days, the fewest number of days possible between the holidays. This has only occurred three times — 2002, 2013 and 2019 — since STR began daily hotel performance benchmarking in 2000. While we will see compression, it is not as meaningful as we would have expected. We expect occupancy between the two holidays to increase by roughly 0.1 percentage points as compared to a year ago with ADR rising 1.8%. Throughout the period, occupancy will remain in the mid-50% range.

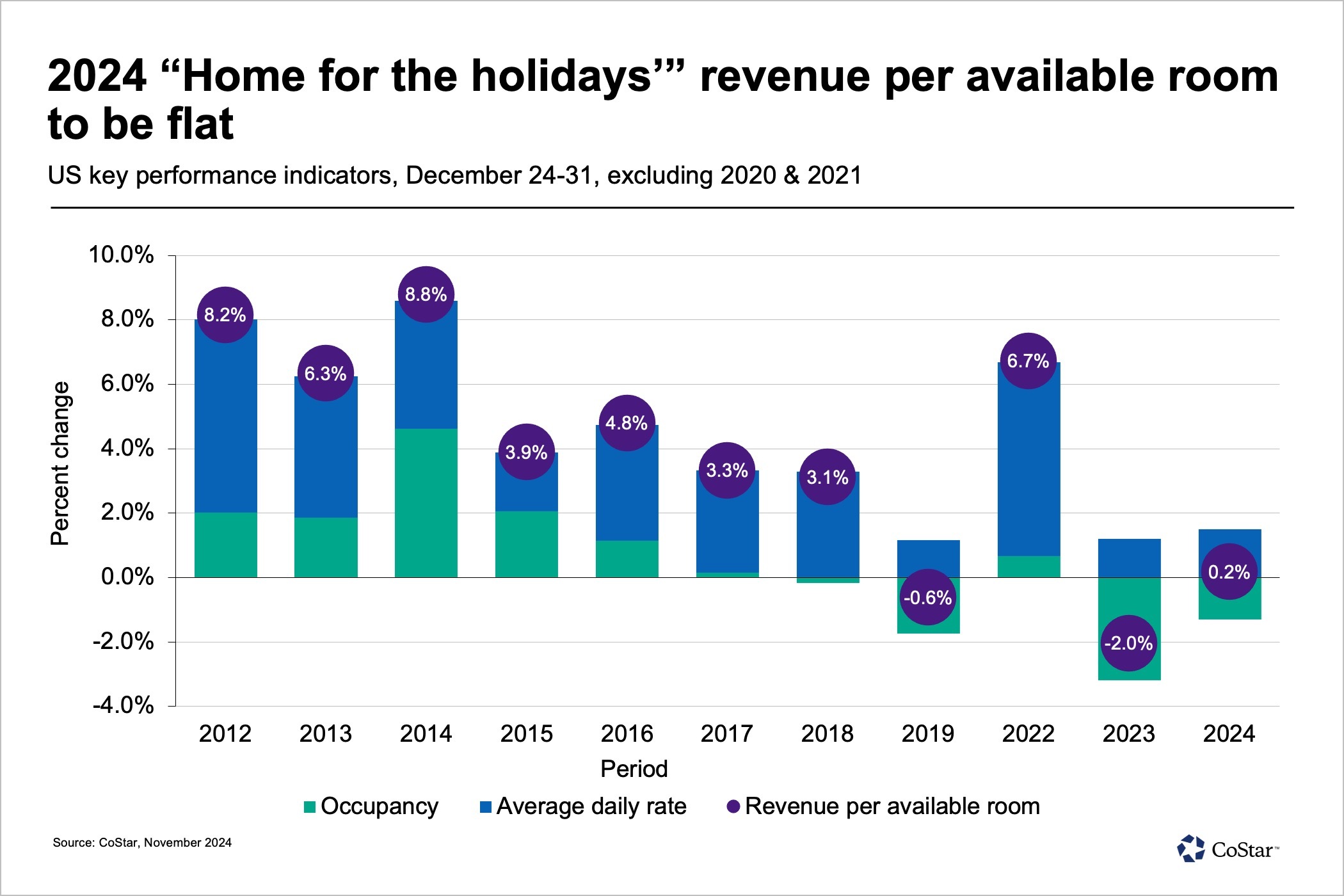

Like the late Thanksgiving, a Wednesday Christmas and New Year’s Day has only happened three times in STR’s historical data, and a move from Monday to Wednesday in one year has never occurred. To determine the impact of this shift, we looked at occupancy between Dec. 24 and 31, the traditional holiday travel period. In 2017, the most recent period when the two holidays fell on a Monday, occupancy averaged 53.4%. In 2019, when Christmas and New Year’s was on a Wednesday, occupancy came in at 52.4%, or 1.3 percentage points lower than the holiday period in 2017. Our projection is for this year’s occupancy to show a similar decrease as compared to 2023 with an absolute average of 50.4%. ADR growth will also be muted, up 1.5%.

Overall, between Nov. 27 and Dec. 31, we expect occupancy to be flat (-0.1 percentage points) with ADR increasing 2%. Thus, the end of year is not anticipated to be jolly, but it also won’t be gloomy — just more of the same.

Isaac Collazo is vice president of analytics at STR.

This article represents an interpretation of data collected by CoStar's hospitality analytics firm, STR. Please feel free to contact an editor with any questions or concerns. For more analysis of STR data, visit the data insights blog on STR.com.