NASHVILLE, Tennessee—Compression nights in hotels across the U.S. peaked in 2015 and have been declining ever since.

external

|

Compression nights are defined as hotels with occupancy levels at 95% or higher, said Jessica Haywood, director of research and development at STR, during a data dive at the Hotel Data Conference. STR is the parent company of Hotel News Now.

Supply and demand are two major factors affecting compression, she said, but it’s affecting hotels more than short-term rentals.

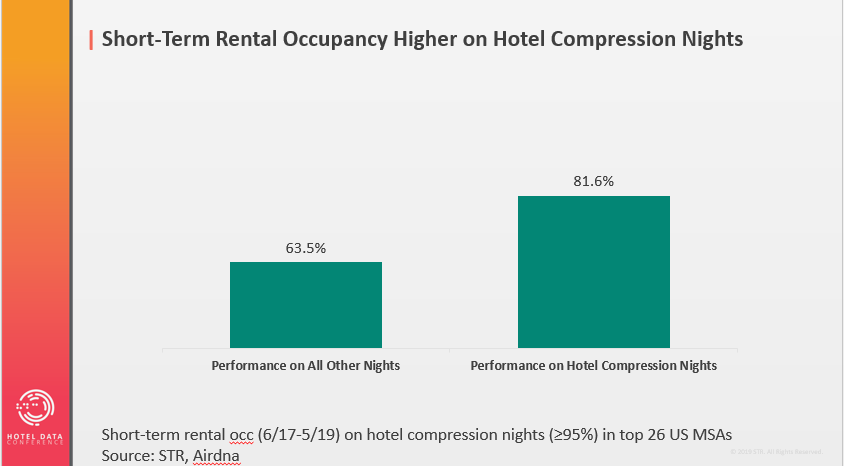

As of May 2019, there have been 50 fewer hotel compression nights compared to 2018, she said, and data shows short-term rental occupancy has been higher on hotel compression nights. The average occupancy of short-term rentals on hotel compression nights is about 82% compared to just 64% on non-compression nights, she said.

Supply of short-term rentals fluctuates and increases during high-demand periods, she said, and if short-term rental supply didn’t increase, it is likely occupancy would be even higher.

Pricing

In terms of pricing power on high-compression nights, hotels in 2018 charged 96% more on rates than on non-compression nights, Haywood said. That is the highest premium seen in the 2000s so far. Despite the number of compression nights declining this year, she said she hasn’t seen any drop in pricing power.

As of 2019, the premium so far for hotels is 74% on high-compression nights, she said.

Short-term rentals are also showing pricing power on compression nights. However, in the last two years through May 2019, the difference in price premiums between compression and non-compression nights for short-term rentals is only 15% compared to 39% for hotels in the top 25 markets, which shows short-term rentals still have a long way to go with revenue management around high-demand times, she said.

It’s possible that the lower rates from short-term rentals might also pressure hoteliers to keep rates lower during periods of high compression, Haywood added.

Segments, location types

Within the segments, Haywood said each one has seen a drop-off in number of compression nights. The biggest declines were in upper upscale and upscale, she said. Since 2015, supply growth in the upper-upscale segment has been 6%, while upper-midscale supply has increased 13%.

Haywood said pricing power in each of the segments, except luxury, have reached record rate premiums. On a year-to-date basis, though, that picture is a little bit different.

For three of the classes—upper upscale, upper midscale and midscale—“we are seeing pretty substantial drop-off so far this year … a lot of compression does happen in the back half of the year, so this trend could reverse,” she said.

She added that it’s important to note that each of those segments also have substantial supply growth.

Looking at the same data by hotel location type, it tells a similar story.

“We are seeing a drop-off in all of the location types, with the biggest drop-off being in airport and suburban hotels,” she said.

Haywood said STR took data from Airbnb looking at 10 major U.S. markets and found that 25% of short-term rental supply is in suburban locations and 6% is in airport locations. She said it’s possible that is affecting the number of compression nights in hotels. However, a total of 64% of short-term rentals are in urban locations and there hasn’t been a substantial drop-off in hotel compression nights.

Price premiums by location type has a similar story to the segments, she said. Revenue-per-available-room premiums in all of the hotel location types, with the exception of resort properties, have seen record highs in 2018. But, again, on a year-to-date basis, things are a bit different.

Rate drops on compression nights were seen in urban, suburban and interstate locations, she said.

Compression nights by market

The top five U.S. markets with compression nights is a good mix of urban and leisure destinations and primary and secondary markets, Haywood said. Those markets include New York; Florida Keys, Florida; San Jose/Santa Cruz, California; San Francisco/San Mateo, California; and Boston.

“There is no single factor that really tells you how a market is going to do in terms of compression,” she said. “It’s really just a mix of different factors (such as events, seasonality and supply).”

If the compression threshold was dropped from 95% to 90%, more markets would experience some level of compression, she said.

When comparing short-term rental occupancy to hotel occupancy in those markets on compression nights, short-term rentals saw higher levels.

Notably, Nashville and Chicago have occupancies of 90% on hotel compression nights, which indicates those markets are “really sold out.” The lowest markets in terms of short-term rental occupancy on hotel compression nights are Fort Walton Beach, Florida, and Myrtle Beach, South Carolina.

Occupancy on hotel compression nights in those markets is around 76%.

“’We think this is because leisure markets typically trend differently than urban markets,” she said.