In the week ending April 12, U.S. hotel revenue per available room (RevPAR) was flat as expected – up just 0.2% – due to difficult comparisons to last year’s solar eclipse as the measure rose 0.2%. Excluding the 16 markets in the eclipse’s path, RevPAR rose 2.8% driven by average daily rate (ADR), which rose 2%.

Hotel markets across the country benefitted from strong group demand along with the continuation of spring break travel. Top 25 market RevPAR – excluding Dallas which was in the eclipse path – increased 2.9% while the rest of the country posted equally strong RevPAR (+2.7%).

The Easter/Passover calendar shift provided a tailwind this week as meeting planners took advantage of availability before the observances begin. Another tailwind this week was spring break with 14% of students out on break, according to STR’s School Break report. However, the start of Passover on Saturday, April 12, affected weekend results, especially in the Northeast and top 25 markets. Even though uncertainty has risen significantly in the last month, hotel demand over the past four weeks is up 1.7%.

Start of the week affected the most by eclipse

A total of 16 hotel markets were in the path of totality of the solar eclipse on April 8, 2024, including Austin, Dallas, San Antonio, Little Rock, Indianapolis, Cleveland, Buffalo and Vermont. During the comparable week in 2025, these 16 eclipse markets – which make up just under 10% of U.S. hotel room supply – saw weekly RevPAR decrease 24.2%, mostly on ADR (-15.2%) while occupancy retreated 7.5 percentage points. Sunday and Monday took the biggest hit with RevPAR declines of 63.7% and 41.4%, respectively. RevPAR turned positive for the group of markets on Wednesday, before returning to negative territory on the weekend. Excluding Sunday and Monday, RevPAR for this group of markets was down 3.2% but ranged from up 52.5% in Indianapolis to down 24.3% in San Antonio. Nine of the 16 saw RevPAR growth after the eclipse comparison.

Non-eclipse markets flip-flopped

Excluding the eclipse markets, top 25 market hotel RevPAR went from increases to decreases as the week unfolded while the rest of the country saw the opposite. Top 25 market RevPAR growth saw double-digit gains from Sunday through Tuesday, slowing on Wednesday (+0.8%) and declining thereafter. The largest decrease was on Saturday (-5.6%) at the start of Passover.

The opposite occurred elsewhere with negative RevPAR on Sunday (-6.1%) and slowly improving throughout the week ending on Saturday, where RevPAR increased 5.1%. Change in ADR had the greatest impact on performance in both market types.

This week’s hotel performance callouts include:

- Orlando achieved the largest RevPAR growth (23.8%) of any top 25 U.S. hotel market, posting double-digit gains across every day. We assume this is a result of spring break travel along with conferences as group occupancy increased 4.5 percentage points.

- RevPAR in San Francisco grew 22.9% this week via the industrial tech conference AVEVA World. Group occupancy in San Francisco also grew 8.1 percentage points, the most of any top 25 market. San Francisco has posted strong group results in the past three weeks.

- Detroit also saw strong RevPAR growth, up 22.2%, benefiting from RAPID + TCT show which was co-located with three other shows. Group occupancy rose 5.3 percentage points.

- Beyond the top 25, strong RevPAR gains occurred in Augusta, Georgia, which hosted the annual Master’s Golf Tournament. RevPAR increased 13%, which is a significant lift given that the comparison is to the matched tournament dates last year. Occupancy reached 86.9% at an ADR of $543, the second highest in the country after Maui Island, Hawaii. But keep in mind, Augusta has been running high occupancy post-Hurricane Helene.

- Other top RevPAR performers included popular spring break markets such as Gatlinburg/Pigeon Forge (+63%) and the Florida Panhandle (+32%).

Group travel alive and well in the top 25 markets

Group demand in luxury and upper-upscale hotels softened this week, increasing just 0.5% following two weeks of double-digit gains. Among the top 25 markets, group demand posted solid gains advancing 4%, following 30% growth in the past two weeks. Last year’s eclipse had little impact to group travel since relatively few luxury and upper-upscale hotels were in the path of the eclipse and the event occurred on a Monday, which is typically a slower-performing day for group travel. Group demand was positive in 16 of the top 25 markets with St. Louis and Las Vegas posting strong group gains. Group ADR in the top 25 markets increased 3.8%.

Over the next two weeks, group demand is expected to decline significantly, due to Passover and Easter, and then return to normal patterns in May.

Eclipse comp had greatest impact on lower chain scales

Bifurcation continued across the hotel chain scales with the largest RevPAR gains in luxury (+4.9%), which rose entirely on ADR. Upper-upscale hotels posted a more modest gain with RevPAR up 1.6%, boosted by both ADR and occupancy. The next four chain scales posted steadily declining RevPAR ranging from down 1.1% in upscale to down 4.6% in economy, with ADR the primary culprit.

While the eclipse comp affected all chain scales, the greatest impact was across the lower four chain scales. Excluding eclipse markets, all chain scales except economy posted positive RevPAR with a relatively small increase in the lower scales, ranging from 1.4% in upscale to 0.4% in midscale. Economy hotels declined 1.1% while luxury rose 6.5% and upper upscale advanced 3.2%.

Canadian border demand affected by eclipse comp

Canadian border comparisons this week were challenging because several Canadian markets were in the path of last year’s eclipse. Detroit, the largest Canadian border market, hosted one of the city’s largest co-located tech conferences. Additionally, the Easter/Passover shift has made an apples-to-apples comparison difficult for both the Canadian and Mexican borders.

Given this complex backdrop, demand across 1,156 hotels within 100 miles of the Canadian border increased 0.1%, compared to national demand (+0.4%). Excluding the eclipse markets, demand was up 7.7% compared to U.S. demand up 1.4%. On the Mexican border, of the 916 hotels within 75 miles, demand was down 3.4%. Tucson and El Paso, the two largest Mexican border cities, posted demand declines of 3.1% and 13.6%, respectively.

Huge events and spring holidays lift global performance

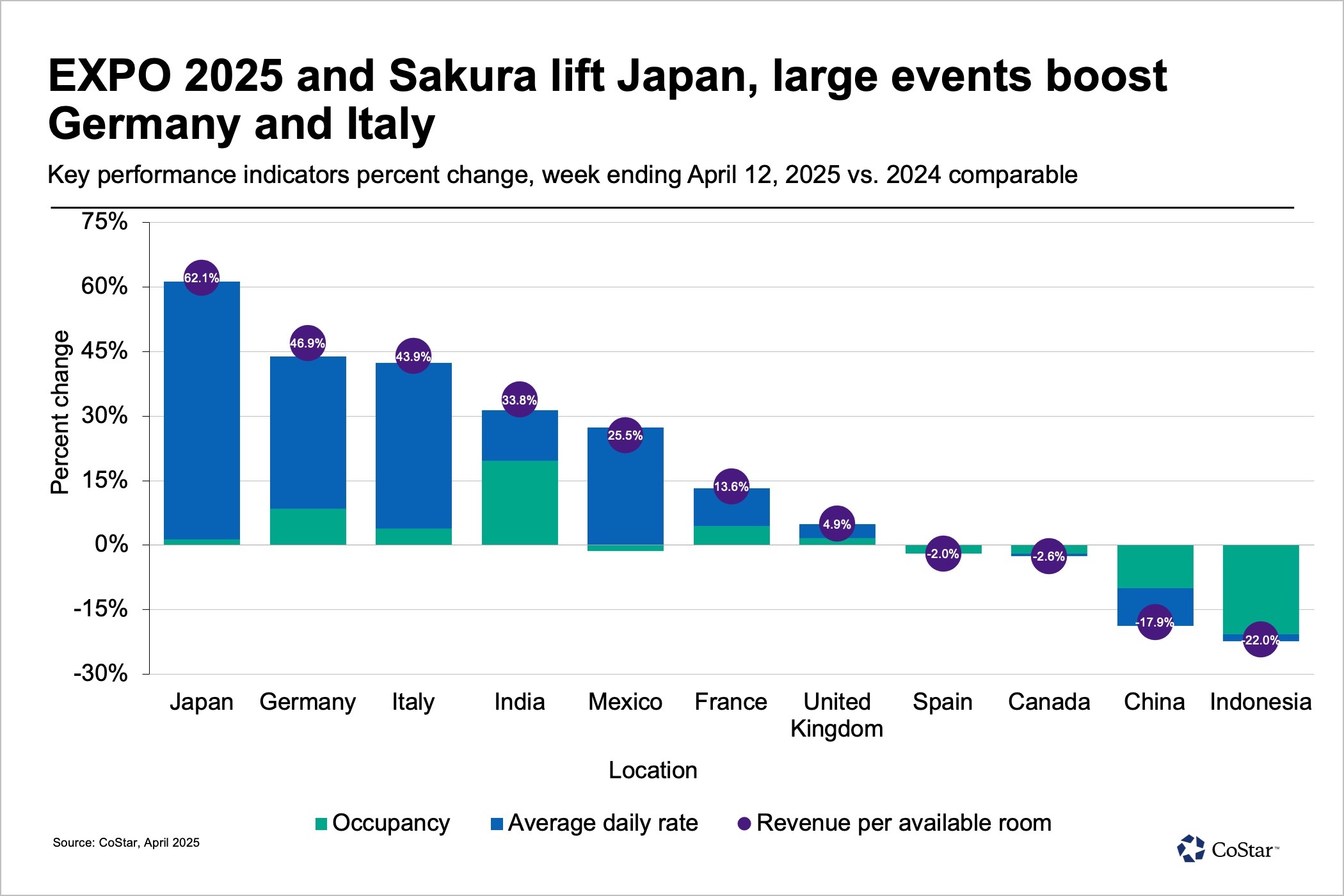

Hotel RevPAR across the globe soared to 12.8%, lifted by major events and spring holidays. ADR almost exclusively drove the increase, rising 12.2%, unlike last week when occupancy played a more significant role in global RevPAR gains.

- Japan took the top spot with RevPAR up 62.1%. The country benefited from the start of EXPO 2025 along with cherry blossom (sakura) season. All Japanese markets posted double-digit RevPAR gains led by EXPO 2025 host city, Osaka.

- RevPAR in Germany rose 46.9% with Munich hosting BAUMA 2025, a trade fair held once every three years touted as being the world’s largest for construction and mining equipment.

- Italy’s RevPAR increased 44% buoyed by Milan, where the annual Salon del Mobile, an international furnishing and design event, took place. Last year the event took place a week later.

- RevPAR was significantly down in China (-17.9%) and Indonesia (-22%) led by falling occupancy.

- Canada was also affected by last year’s eclipse. RevPAR decreased 2.6%. Excluding the three Canadian eclipse markets – Toronto, Montreal, Niagara Region – RevPAR was up 4.3%.

Looking ahead

Hotel performance will slow over the next two weeks due to Easter and Passover. Last year the two religious observances occurred at different times. This year the impact is expected to be more pronounced. Further out, forward bookings in top U.S. markets for the week ending May 3 are up 4.5% according to STR’s ForwardSTAR. Overall bookings for May and June are up around one percentage.

The religious holidays will also impact many countries outside the U.S., ending the streak of double-digit RevPAR gains for now.

Isaac Collazo is senior director of analytics at STR. Chris Klauda is director of market insights at STR.

This article represents an interpretation of data collected by CoStar's hospitality analytics firm, STR. Please feel free to contact an editor with any questions or concerns. For more analysis of STR data, visit the data insights blog on STR.com.