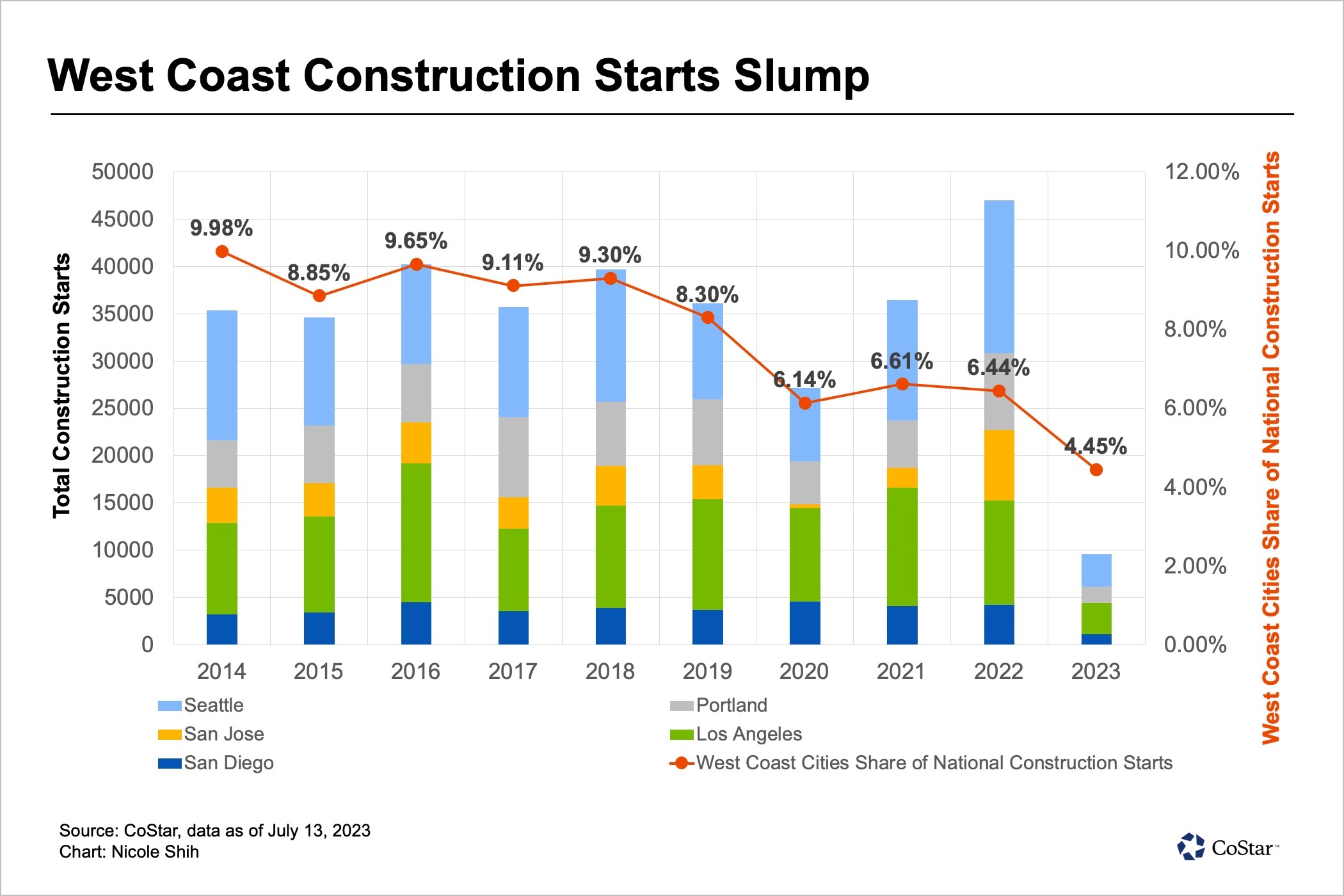

Up and down the West Coast, apartment construction sites are falling quiet despite high demand in a worsening housing shortage.

Fewer multifamily projects have broken ground this year from Seattle to San Diego in one of the slowest starts to apartment construction in a decade. In San Jose, no apartments have broken ground after more than 7,000 started construction last year. In Seattle, 3,433 apartments started building in the first six months, a drop of nearly 60% from the same time last year.

Analysts and real estate executives are already preparing for the lack of building in coming years because apartment construction can't simply catch up later with projects taking roughly two years to build. Eric Bolton — CEO of Tennessee-based Mid-America Apartment Communities, one of the nation's biggest apartment owners — said at a real estate conference last month in New York that by 2024 or 2025 the drop in apartment construction will mean demand further overshooting supply.

"The market gets very nervous about supply pressure," he said, adding that he expects the need will grow in years to come on the West Coast.

Multifamily construction starts are also falling nationally because rising interest rates make it more difficult for developers to build profitably. The West Coast, though, stands as an outlier to other faster-growth Sun Belt markets where construction continues at a faster clip. That's not only because of demographic shifts but also partly because of red tape and high construction costs developers face building in California, Oregon and Washington.

The lack of apartment construction on the West Coast inevitably will cause increased housing prices, further making apartment renting out-of-reach in some of the costliest places to live in the world. That's because, unlike fast-growing Sun Belt markets, even the robust apartment construction of recent years is at a lower percentage of the total overall number of apartment units in West Coast cities.

"It's the worst thing that could be happening," said Jay Lybik, national director of multifamily analytics at CoStar Group. "The region still doesn't have enough housing."

To be clear, the high-growth West Coast cities have been losing momentum since the pandemic began with many experiencing population declines and job relocation to other parts of America. While rents remain at record levels, the growth of apartment rents has been cooling because of economic uncertainty and job contraction on the West Coast.

Here's a look at how the slowed construction is playing out across some West Coast cities.

Los Angeles

A surface level parking lot in Los Angeles' North Hollywood neighborhood gives little indication it's the future site of one of the city's largest apartment construction projects in decades.

Developer Trammell Crow was supposed to start in third-quarter 2022 on District NoHo, a 2 million-square-foot, mixed-use project that was planned feature about 1,500 apartments wrapped around the North Hollywood transit hub at Lankershim and Chandler boulevards.

However, the project's development team, which includes LA Metro, revealed in June that it wanted to decrease the project's total units and commercial space in response to the changing economic climate. A memo dated June 2 blamed "rising construction costs and the increasingly uncertain climate for capital sources to fund the Project" when the developers tried to bring add more income restricted units to the development.

Rising interest rates are the biggest reason apartment construction isn't happening as much this year as in years past in Los Angeles, said Chris Tourtellotte, managing director of LaTerra Development, which isn't involved in the North Hollywood project but is one of the most active apartment builders in greater L.A. Rising interest rates and the crisis at some U.S. banks this year have made it challenging to secure the necessary financing to toss dirt.

"Most developers are having a difficult time closing construction loans," Tourtellotte said.

Tourtellotte said his firm, though, isn't pausing and forecasts that 2025 will be a good time for some developers to complete buildings in greater L.A. due to the lack of competition. LaTerra expects to have a pair of projects completed that year. The company has been able to move projects forward because it has access to competitive debt funding capital and banks that are still lending to developers. It also is developing on land it owns and has entitled.

Kevin Newman, CEO and creative director of Costa Mesa-based apartment architect Newman Garrison + Partners, has been hearing from developers about the painful economics of building right now. One developer client said that they've talked with 60 lenders and still can't get the financing to move forward.

Newman, though, is optimistic about construction levels rebounding by the end of next year as capital markets and interest rates ease. That means a bevy of new supply could be coming online starting around late 2026.

"We could see going back to 2021 levels" of construction, Newman said.

David Evans, a multifamily investment sales broker at Kidder Mathews in Los Angeles, said he isn't as optimistic that Los Angeles rents will rise at a faster clip in 2025. Asking rents in greater Los Angeles are up less than 1% year over year after peaking at a one-year increase of 7.4% in first-quarter 2021, according to CoStar data. The 10-year rental growth market average is about 3.2%.

Evans said some renters are getting priced out of the city while other some L.A. markets are seeing too much construction, which may lead to an oversupply of units.

"Unless there's some dynamic job growth, those buildings aren't going to get filled up," Evans said.

Silicon Valley

Job and income growth had never been an issue for the tech-concentrated Silicon Valley area as both fueled record amounts of multifamily development across the region. Yet even before widespread layoffs, a tightened financing climate and unpredictable economy layered stress on the market's outlook over the past year, there was another culprit that set the stage for little to no development activity: exorbitant construction costs.

"Construction costs got to a point when everyone's pro formas got turned upside down," Erik Hayden, the founder of San Jose, California-based development firm Urban Catalyst told CoStar News. "The Bay Area has some of the most expensive construction costs in the whole world. Add in COVID, and add in interest rate increases, and that financing has become more challenging, and it really doesn't help."

Developers have long chased after record rent growth and strengthened demand across the Silicon Valley housing market, home to some of the nation's most expensive neighborhoods, despite the challenges and high costs associated with new construction. More than 8,300 multifamily units are currently underway, according to CoStar data, the most reported over the past 15 years.

But that pipeline is drying up as financing for projects — which are becoming more expensive to build — is getting harder to secure.

Third-party lenders, a source of financing Silicon Valley multifamily developers often depend on to capitalize projects, have scattered in recent months, Hayden said, making it more challenging to get those proposals off the ground.

"There was a lot of positive momentum coming out of COVID, and in early 2022, we saw financing markets pick up in a big way," the Urban Catalyst executive said. "But by the end of last year [lenders] dropped projects because of inflation and economic uncertainty. It looked like were in the clear, but since then, things have gotten worse. We've all heard them say, 'we're pencils down now, but after the Fourth of July we'll have more confidence in the market and we'll start lending again.' There is a lot of speculation that things will be better in the second half of this year, but I haven’t seen that happen yet."

After projects with more than 500 units each went under construction last year, the San Jose market, which encompasses Silicon Valley, has reported no new housing starts for all of 2023, according to CoStar data.

For Urban Catalyst, which has a San Jose-focused development pipeline valued at more than $1.5 billion, the financing challenges has meant the firm has had to adjust its game plan for two multifamily projects it had initially planned to break ground on sometime this year after landing approvals in late 2022.

It recently kicked off efforts to line up capital for its high-rise Echo apartment tower and have decided to self fund the construction for its Aquino @ Downtown West project. Both would collectively add more than 635 units to downtown San Jose, an area where rents for higher-end units can easily command upwards of $4,000 per month.

While Hayden said he's hopeful that construction on both projects can start next year, he's willing to wait in order to land the right terms.

"There has been a tidal wave of debt equity funds that have come out of the market, but those charge a much higher interest rates and are typically very risky," he said. "If you don't meet what your proforma says, you have the possibility of losing all the equity you put into the project. That's a risk we don't want to take."

While there are plenty of multifamily construction sites throughout the Bay Area that have been arrested by a challenged financing landscape, real estate executives know its a short-term issue. Multifamily rents across Silicon Valley are poised to climb even higher, according to CoStar analysis, making it easier for developers to leap over any temporary economic hurdles to capitalize on the growing market.

"There will be a lot more pro formas that will pencil if rents go up over the next 10 years," Hayden said.

And as rents go up and financing markets begin to ease, housing start figures will follow closely behind. That is, Hayden said, until construction costs once again pull everything right back again.

San Diego

"Construction activity has remained relatively consistent in San Diego, which is to say that it has not been enough," said Joshua Ohl, senior director of market analytics for CoStar Group in San Diego.

The San Diego region has seen some of the state's highest rent growth during the past year at 2.7%, and its vacancy rate is historically low at 3.5%. The approximately 8,000 multifamily units under construction represent about 2.9% of total regional inventory, but the bulk of those apartments are high-end units concentrated in downtown San Diego, rather than spread throughout the region.

Ohl said most regional estimates suggest San Diego should be adding 15,000 total housing units annually. But the region typically tops out around 8,000 multifamily units, with single-family units adding about another 2,000 annually.

"Construction starts have remained stubbornly low in recent quarters following the rapid rise in interest rates coupled with the rise in cost for most construction materials," Ohl said. "San Diego could feel the impact of even fewer supply additions in the coming years with fewer properties going vertical in the present."

Inland Empire

California's Inland Empire has long been known as a relatively more affordable region for residents who commute to work in more expensive regions including Los Angeles and San Diego. Inland apartment construction has paced ahead of its Southern California neighbors in recent years, but the region is not immune to rising rents and construction costs.

"Developers were enticed to initiate construction by a rapid jump in rent potential from pre-pandemic levels," said Jesse Gundersheim, senior director of market analytics for CoStar Group, who tracks the Inland Empire.

He noted current construction in the Inland Empire, at about 6,400 units, amounts to 3.8% of existing inventory. That's ahead of California's statewide average, but lags behind the national average of 5.6% of existing inventory.

"Meanwhile, demand has been uneven," Gundersheim said. "Occupancy is growing again but contracted over the past year." The region's apartment vacancy rate is at 5.4%, above historical averages, and appears to be heading higher.

Developers could be discouraged to build more Inland apartments beyond the coming year, based on rising vacancy rates and rents that grew by a slim 0.3% over the past 12 months.

"The substantial amount of apartment construction scheduled for delivery over the next year is forecast to outpace demand growth," Gundersheim said.

Seattle

Seattle has logged some of the strongest annual growth in housing starts of any major West Coast urban area over the past two decades.

But despite housing construction that still hovers near record levels, Emerald City — and Washington as a whole — are still falling behind in building new housing for its booming population.

The region has added an average of nearly 10,000 multifamily units annually over the past decade and about 28,000 units are under construction this year, CoStar data shows.

“Jobs and population grew faster than housing in the 2010s, and we’re still playing catch up to some extent,” said Elliott Krivenko, CoStar’s Seattle market analyst.

That said, the pipeline of new projects has dried up. The number of housing permits in Seattle declined more than 25% over the 12 months ending May 1 — by far the biggest drop among such big West Coast cities as Los Angeles, San Francisco and Portland, according to the data.

This year’s decline comes at the worst possible time for Seattle, which recently reclaimed its title as the fastest-growing big city in the United States by population. The city added 17,750 people in the 12 months ending July 1, 2022, for a total population of just under 750,000, according to U.S. Census data released in May.

Seattle’s 2.4% population growth rate was the fastest among the 50 largest cities, easily beating the Sun Belt boom towns that round out the top five fastest growing: Fort Worth, Texas; Charlotte, North Carolina; as well as Miami and Jacksonville in Florida.

Seattle’s King County will need to add almost 17,000 new homes a year for the next two decades to keep up with that growth, according to state Commerce Department projections this year.

The housing deficit extends across the Evergreen State. Washington has added an average of about 35,000 housing units per year over the past decade, according to state data — well short of the projected 55,000 per year totaling more than 1.1 million new homes needed over the next 20 years, according to the forecast.

Still, Washington’s legislature this year has passed more than a dozen bills aimed at boosting housing supply in a state where it’s expensive.

Washington joined Oregon and California in overhauling single-family zoning to increase apartment density and address a worsening housing shortage that proponents say has contributed to rising affordability concerns and homelessness.

The legislature and Gov. Jay Inslee also pushed through laws that make it possible to permit and build more accessory dwelling units and streamline local permit and development regulations.

“We have extremely long timelines for building large projects and many proposals never see the light of day,” Krivenko said. “But compared to Portland or some California cities, it may be a bit easier to get projects out of the ground and have them pencil out.”

Portland

Portland, another Pacific Northwest tech stronghold, has been losing net population just as multifamily development has ramped up.

Rose City lost more than 8,000 people last year for a 1.3% decline, ranking 47th among the 50 largest cities for population changes, according to the May census data.

As people leave Portland for other parts of the country, the city's multifamily construction pipeline has expanded over the past two years to 8,700 units. That will boost the region’s apartment inventory by about 4% as developers finish a wave of mostly luxury units in coming months, said John Gillem, CoStar's market analyst in Portland.

However, like other West Coast cities, Portland’s apartment starts have slowed dramatically this year.

Just over 1,560 units began building in the first half of 2023 after about 5,000 kicked off construction in the same time last year. Over the past 12 months, apartment starts have fallen almost 37% from the prior year period to less than 4,650 units, CoStar data shows.

Meanwhile, apartment leasing has cooled dramatically from its record-setting levels of mid-2021, contributing to an increase in the greater Portland's vacancy to 6.5% from under 5% a year ago. CoStar projects that the region's apartment vacancy rate could reach 7.4% by the end of the year, the highest in nearly 20 years.

The latest data suggests the pace of multifamily permits pulled in the region this year may surpass the 2021 mark of about 6,500 units.

"This means more units will be hitting the market in the coming quarters in the face of dwindling demand," Gillem said.