CoStar News catches up with Cristina Garcia-Peri, senior partner and head of strategy and corporate development at Azora, to discuss where the Madrid-based investment manager with €6 billion of residential, hospitality, office and logistics assets under management will be allocating capital this year, its second hospitality fund and the mood at Mipim. This interview has been edited for length.

What are you expecting the mood to be at the Mipim real estate conference this week given the turbulence in the market over the past year?

The mood at Mipim is going to be twofold. Investors are still expecting values to continue to fall so there is going to be a lot of caution and a lot of discussion about where inflation is going and what are the risks if it doesn’t flatten, and interest rates continue to rise. Most investors are still on the sidelines and still unclear about where things are going to settle.

The second sense is that we are not going to return to the same low interest rate environment that we had before for a very long time, and I think that is a good thing. The correction is going to be painful; it won’t be the same across different asset classes, but I think when you look back over the past five or six years, capital has been allocated wrongly. In certain strategies you were not getting enough return for the risk taken. There was the sense that there was no alternative: bonds and fixed income were not an alternative, lending was not an alternative so where did you look for long-term stable cash flows? Real estate and infrastructure. As a result, there has been quite a lot of misallocation of capital, particularly in the more core, core-plus strategies but also in value-add strategies because, even as returns were coming down, everyone was accepting lower returns for exactly the same risk.

At Azora, we had already started to slow down our pace of investment, even before the correction, because we were no longer comfortable with the risk-return. I think an environment where rates are not at zero is healthy for everyone and yes, as real estate investors we now have more alternatives, but I think that will allow us to focus again on what real estate actually is and what it can really do for an investor’s portfolio. We will be going back to things like location, location, location – which is a really simple way to judge whether a real estate investment is good or bad – and really thinking about supply and demand dynamics and rental growth as the main driver of returns rather than simply looking at yield compression.

A lot of investments have been made on the back of yield compression and falling interest rates and always chasing the next investor who still doesn’t own real estate in a particular country or sector and who is willing to accept the risk for a slightly lower return and that has been the story for the last cycle.

In the new cycle, investors will be more selective and discerning and really go back to asking themselves "do I believe there will be rental growth for this asset?’’, and what are the drivers behind this? Is demand growing or is it because I am going to improve the asset and people will be willing to pay more for it. Some of these basic things have almost been ignored or forgotten – and that is why the new environment will be more healthy, certainly for investors like Azora because we are a value-add investor – so a good investment for us always starts with paying an attractive price.

Now that real estate has to compete with debt for the first time in a very long time, institutional investors have reached their allocation limits and interest rates and financing costs are looking to stay higher for longer – what opportunities are arising from these recent changes?

There will definitely be opportunities and it goes back to what I was saying before – what does real estate add to your portfolio as an investor? Fixed income and bonds are not linked to inflation – so that is one thing real estate continues to have: your leases are in some way linked to inflation so real estate will continue to be a very good inflation hedge.

Secondly, real estate has this scarcity that in general bonds do not have – governments have proved to us all that their ability to issue debt is infinite, whereas real estate is not, which links back to my point about location location – if you own an asset an asset in a place where nothing else can be built around it you know that the supply of that asset is limited. Owning an asset in the Champs Élysées in Paris or in Mayfair in London, for example, is unique – there is always going to be a value assigned to that asset.

The other difference real estate has from bonds, and potentially from infrastructure, is that it gives you the ability to continue to increase the returns and your ability as an investor and manager to really have an impact of the return. If you buy a bond you just sit on it, yes you can trade it but that is a different matter. Even if you buy an infrastructure asset you normally have a highly regulated return. If you buy a student house or a residential asset or hotel and you manage it – your ability to improve that asset, to attract more clients and to increase rents because you are providing more value is extremely large and your ability to improve its value while you own it is much larger.

With regards to supply and demand there are still huge supply needs in the real estate sector – the need for housing and affordable housing is massive, the need for student housing, flexible housing and housing for seniors whether it be nursing homes or assisted living is immense because the speed at which Europe’s population is aging is extremely fast, there just isn’t enough stock. Demographic changes in terms of the needs of how populations are evolving forces you to reimagine and reinvent cities, and change asset to new uses and start mixing uses, and I think these are all areas in which there will be exciting opportunities.

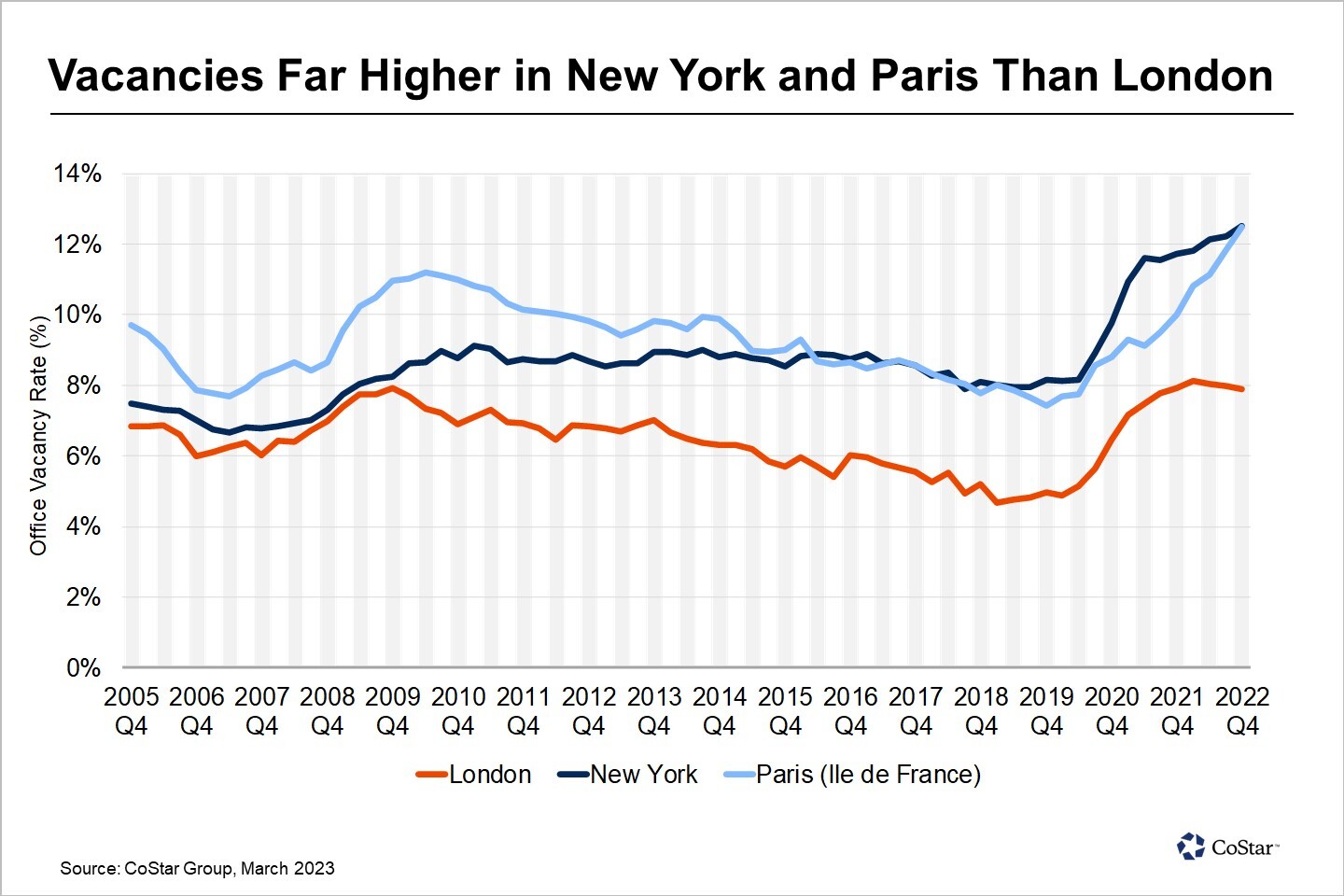

You said at the start of 2022 that the office market would come back with vengeance over the course of the year, have you seen that come to pass?

For me in the office sector we will see a pendulum effect. We have dealt with COVID and the advent of technology like Zoom and Teams, but as we all work from home I think we all realise that a company is not a made of people working individually working in their homes, it’s made of people working together and that instils a sense of company culture, a sense of belonging and the loyalty of employees – these are all things you cannot experience by working from home. I think corporates are starting to realise that if employees work from home too often they miss out on that sense of belonging and loyalty and the ability to collaborate and foster creativity – you need people to talk and brainstorm together.

For all of these reasons I think the office will come back but it will be a different type of office – they will need to be in a premium location with access to public transportation and foster employee wellbeing so that workers find them attractive and want to come into the office rather than working at home. All of this is opening up an opportunity to refurbish offices in good locations and these assets are going to be extremely attractive. The polarisation of valuation and attractiveness between quality, well-located offices and poor quality assets in bad locations is going to be immense.

Of course all markets are different and the US is very different to Europe – for example in New York , the amount of office space that you have is too much, and secondly, and this hasn’t happened in Europe, in the US they had what they call the "great resignation". A lot of people after leaving the city during lockdown realised that they didn’t want to go back to commuting two hours a day and they can live in their home towns where life is significantly cheaper and they don’t have the stress and pressure. It is still very expensive to refurbish offices in the US, so eventually there will be opportunities to buy, especially when owners who must refinance and can’t decide to hand over the keys as Brookfield did with an asset recently.

Over the past cycle, buyers were able to buy assets or portfolios using huge amounts of leverage to get the high returns they needed. Now debt costs have gone up they can’t do that anymore and those buyers have disappeared from the market, which is contributing to the drought in deals we have seen over the past year.

What is happening now is very different to what happened post 2008 – back then there was an issue with the banking system, which has been resolved, so this time around you are not going to have a massive amount of assets coming to market all at once. You need to find motivated sellers. For example someone who bought an asset in Germany at yields below 3% and got finance at 1% and who is facing refinancing right now, can either put in more equity and repay the debt or sell the asset because their cost of financing is probably too high for the current and expected yield of the asset.

There will also be banks that need to sell assets as they are under incredible pressure not to increase [non-performing loans] and the moment an asset looks like its going to turn bad they will sell the loan exposure. Then there are corporates, all of them potentially selling assets to reduce debt levels so I am convinced we will see more REITs on the continent selling assets and we will see more developments that are paused because the owners can’t get financing. We are also going to see assets that are stranded from an ESG point of view. The trick at the moment is to be very patient, wait for the right opportunity and motivated seller and be ready to act.

We are big believers in investing on the back of mega-trends, but in circumstances such as now and like in 2013, you also need to have a portion of your capital set aside to be ready to react to the opportunities. I think it will be a quiet first half and then I think two things will happen. As time goes by there will be more clarity for investors about the future of rates and inflation and more pressure for motivated sellers to sell. As time goes on long term investors are going to ask themselves "do I really want to get the last penny on the table?" and we will see many of them coming back to the market to start buying, patiently as there may be some more correction, but they will start coming back. We are going to go through a period of patience but as we get to the summer, capital will start to deploy again.

Following the launch of Azora Exan in 2021, can you give a run through of what the JV has been doing and how the US investment market has performed vis-a-vis Europe?

The US market always adjusts much faster than Europe: when prices correct, sellers immediately take the hit and move on. It is also such a huge market. We spoke earlier about offices in New York but let me tell you about Miami, because that market is booming. Companies were moving there not just post-COVID but before the pandemic hit, lured by lower taxes, lower cost of living, better weather and lower office rents compared with your big cities like New York, Chicago and Los Angeles for example.

Exan is based in Miami and has a huge ability to source deals in the Sunbelt States [18 states across the Southern US] among some of the largest real estate asset classes such as offices, retail and logistics. So we are continuing to grow that business and are also bringing in our expertise to look at more operationally intense asset classes such as residential, hospitality, student housing and senior living in which Azora is very active in Europe.

Can you give an update of how much has been deployed by the European Hospitality Fund since its launch in 2021 and how has assembling the portfolio differed from a few years when Azora was assembling Hispania, which it eventually sold in 2018 generating net returns of 19% internal rate of return.

The fund is 75% committed, 33% is in Spain, 27% in Portugal, 24% in Italy and the rest across Germany, Greece and Belgium. Geographically it is very well balanced and we will continue to grow in Greece in particular which is a little underrepresented. From a mark to market point of view right now we are at a mid-twenties net return for investors, which is above our target of 12 to 14%. Some of that will dilute itself but we are very confident that we are are going to outperform our targets and deliver a very strong return.

Part of the portfolio is stabilised with yield on cost of about 9%, but parts of the portfolio are still in ramp-up which is good news because this will continue to add to these returns. We are very pleased with the fund and already working on fund two.

For the current fund we will finish investing at the end of the year and we have approximately eight years from first close in 2020 to exit, so we have plenty of time to continue to manage the assets. The portfolio is big enough and of enough quality to offer several interesting alternatives to generate liquidity for the current investors, including a possible IPO. The asset class has become very institutionalised and is still very underrepresented in institutional investors’ portfolios so we are confident that there will be many interesting buyers if and when the time comes.

What has been your experience as a woman in the world of real estate investment, an industry still dominated by men and what can be done to attract more women into the field?

Real estate is still very male dominated but I have seen a big change since I started my first job prior to my MBA in the early 90s when you could still find some people who were chauvinist and there were some biases. I started in real estate in 2011 and I honestly can say I have never faced a single gesture of discrimination or people looking down on me. I don’t think there is even an unconscious bias against women in the sector but I do think as an industry we still have an issue attracting women.

The biggest challenge for the real estate industry is that there are not many women at the top and young women will look at the sector and wonder why that is. We need to make a bigger effort to attract young women and I think part of it needs to come from showing some of the great attributes of real estate as a business, in that you have a great combination of it being a very rigorous and financially driven world and at the same time offering the possibility to have great impact given that you’re building cities and assets where people live, and work and study and it’s fundamental to the growth and wellbeing of our society.

The industry is still facing the same issues with retaining female talent as those I faced during my 30 year career which is reconciling your family life with your work – that is the single most important reason today you don’t see that many women at the top – when you start having children it’s very very difficult , even if you have help from family or nannies, the fact is you are not there and the trade-off between your work and your children is always.

If a woman decides to dedicate herself to her job, that is easy and that was for many years my case, but at some point I knew where my priorities had to be and I took a five-year sabbatical. The challenge for a woman who needs to take a step back for a few years or for the rest of her professional career is that if you have been a high performer, it is very hard to stay motivated because you feel you might never get back to that level you had before and you may feel that everyone is looking at you like a lame duck. And that is where a lot of women decide to leave. The challenge for companies is how to keep that female talent motivated while they take a step back. There has been tremendous progress and some companies are now much better at giving flexibility and support and much more creative in designing attractive career paths for those women. But there is still big room for improvement and we as women, should try to push our companies into getting better at this and support all younger women as much as we can.

article9 Min ReadMarch 16, 2023 10:49 AMLocal leaders discuss investor appetite amid economic headwinds.

article9 Min ReadMarch 16, 2023 10:49 AMLocal leaders discuss investor appetite amid economic headwinds. article1 Min ReadMarch 16, 2023 07:06 AMCoStar News and sister publication Business Immo team up to quiz the leader of the region around Paris.

article1 Min ReadMarch 16, 2023 07:06 AMCoStar News and sister publication Business Immo team up to quiz the leader of the region around Paris.

article2 Min ReadMarch 16, 2023 06:20 AMParters commit to Joint Venture To Improve Birmingham's Knowledge Quarter

article2 Min ReadMarch 16, 2023 06:20 AMParters commit to Joint Venture To Improve Birmingham's Knowledge Quarter article1 Min ReadMarch 16, 2023 05:49 AMThe IWG chief executive says commuting is 'one of the craziest inventions of the last 100 years' and on the ropes anywhere it is long, inefficient and expensive.

article1 Min ReadMarch 16, 2023 05:49 AMThe IWG chief executive says commuting is 'one of the craziest inventions of the last 100 years' and on the ropes anywhere it is long, inefficient and expensive.

article2 Min ReadMarch 16, 2023 05:10 AMMoney is not an issue for the US property owner and developer after Stone Point Capital became involved last month.

article2 Min ReadMarch 16, 2023 05:10 AMMoney is not an issue for the US property owner and developer after Stone Point Capital became involved last month.

article2 Min ReadMarch 15, 2023 06:10 PMGlobal markets were rattled by the big bank's troubles, prompting attendees at the Mipim property conference to ponder the impact on their industry.

article2 Min ReadMarch 15, 2023 06:10 PMGlobal markets were rattled by the big bank's troubles, prompting attendees at the Mipim property conference to ponder the impact on their industry.

article1 Min ReadMarch 15, 2023 10:55 AMYoung is moving from London as group looks to double in size across the region.

article1 Min ReadMarch 15, 2023 10:55 AMYoung is moving from London as group looks to double in size across the region.

article1 Min ReadMarch 15, 2023 08:37 AMJames Porter moves from managing director - occupier solutions.

article1 Min ReadMarch 15, 2023 08:37 AMJames Porter moves from managing director - occupier solutions.

article1 Min ReadMarch 15, 2023 07:07 AMCity centre site is destined for mix of housing units and sits close to railway station.

article1 Min ReadMarch 15, 2023 07:07 AMCity centre site is destined for mix of housing units and sits close to railway station. article2 Min ReadMarch 15, 2023 06:48 AMExperts cite North East's Newcastle Helix scheme as an example of successful city centre regeneration around higher education.

article2 Min ReadMarch 15, 2023 06:48 AMExperts cite North East's Newcastle Helix scheme as an example of successful city centre regeneration around higher education. article1 Min ReadMarch 15, 2023 06:18 AMHorrell also talks to CoStar News about sector opportunities, getting deals done and how the Chancellor could help business growth.

article1 Min ReadMarch 15, 2023 06:18 AMHorrell also talks to CoStar News about sector opportunities, getting deals done and how the Chancellor could help business growth.

article5 Min ReadMarch 14, 2023 09:36 AMVacancies have stabilised at lower levels in London but yields are rising.

article5 Min ReadMarch 14, 2023 09:36 AMVacancies have stabilised at lower levels in London but yields are rising.

article3 Min ReadMarch 14, 2023 09:21 AMCushman report warns that a combination of factors means landlords must act now.

article3 Min ReadMarch 14, 2023 09:21 AMCushman report warns that a combination of factors means landlords must act now.

article2 Min ReadMarch 14, 2023 07:32 AMDeal includes 64% of stake in Icade Santé and Icade Healthcare Europe's portfolio of assets.

article2 Min ReadMarch 14, 2023 07:32 AMDeal includes 64% of stake in Icade Santé and Icade Healthcare Europe's portfolio of assets.

article1 Min ReadMarch 14, 2023 05:41 AMThe commercial and residential agent is launching a dedicated BTR division at the real estate conference.

article1 Min ReadMarch 14, 2023 05:41 AMThe commercial and residential agent is launching a dedicated BTR division at the real estate conference.

article2 Min ReadMarch 14, 2023 05:02 AMThe duo has teamed up with transport group Ascendal to announce the plans at the Mipim conference.

article2 Min ReadMarch 14, 2023 05:02 AMThe duo has teamed up with transport group Ascendal to announce the plans at the Mipim conference.

article13 Min ReadMarch 13, 2023 10:25 AMCristina Garcia-Peri, senior partner and head of strategy and corporate development at Azora, catches up with CoStar News.

article13 Min ReadMarch 13, 2023 10:25 AMCristina Garcia-Peri, senior partner and head of strategy and corporate development at Azora, catches up with CoStar News.

article1 Min ReadMarch 13, 2023 06:20 AMThe transaction for the Pullman Cannes Mandelieu Royal Casino has completed as the world's biggest real estate conference gets underway in the city.

article1 Min ReadMarch 13, 2023 06:20 AMThe transaction for the Pullman Cannes Mandelieu Royal Casino has completed as the world's biggest real estate conference gets underway in the city.

article2 Min ReadMarch 13, 2023 05:38 AMThe acquisition of a majority stake in Germany's Redos enables it to create a huge retail warehouse park portfolio.

article2 Min ReadMarch 13, 2023 05:38 AMThe acquisition of a majority stake in Germany's Redos enables it to create a huge retail warehouse park portfolio.

article4 Min ReadMarch 12, 2023 07:56 AMThe UK minister for investment, a US economics star and Amanda Staveley to be among speakers as 23,000 prepare to descend on Cannes for the world's largest real estate conference.

article4 Min ReadMarch 12, 2023 07:56 AMThe UK minister for investment, a US economics star and Amanda Staveley to be among speakers as 23,000 prepare to descend on Cannes for the world's largest real estate conference.