It was a rough week for the U.S. hospitality industry. Hotel demand varied due to groups and business travelers being absent because of holiday shifts and displaced residents seeking shelter from hurricanes.

On the heels of strong gains the previous week, U.S. hotel performance for the period ending Oct. 5 showed the effects of Rosh Hashanah and Columbus Day/Indigenous Peoples Day calendar shifts as well as the impact of Hurricane Helene. Revenue per available room dropped 7.7% year over year with average daily rate retreating 4.4% and occupancy falling 2.3 percentage points.

All days of the week showed declining hotel RevPAR with decreases accelerating Wednesday — the start of Rosh Hashanah — and the largest declines coming from hotels located in the Western U.S., where RevPAR fell 10.1%. The impact was especially pronounced in Las Vegas (-25.9%), which saw group demand fall 16.5%. Additionally, with the weekend ahead of Columbus Day/Indigenous Peoples Day included in the comparable period last year, weekend RevPAR fared worse. Hotels in the Northeast U.S. also saw a sharp decrease in RevPAR (-7.1%), but unlike the total U.S., the largest drop for those markets occurred on weekdays (-9.5%).

Hurricane Helene and subsequent resident displacement into hotels also had a major impact on hotel performance. While room demand decreased between 3% and 5% across eight of the nine U.S. census regions, the South Atlantic experienced a demand increase of 1.7%, with most of the increase in North Carolina, South Carolina and Georgia, where Hurricane Helene had the most impact.

Specific markets in the path of Hurricane Helene and the resulting flooding were Columbia, South Carolina; Macon/Robbins, Georgia; Florida Central North; Augusta, Georgia; Sarasota, Florida; and Charlotte, North Carolina; posting RevPAR gains of 25% year over year. Occupancy gains year over year exceeded 15 percentage points in all markets except August. Hotels in hardest hit Asheville, North Carolina, were down significantly; however, it is difficult in this early stage to accurately represent hotel performance given the extensive damage to property in the area.

All hotel chain scales posted RevPAR declines with the top three affected the most by calendar shifts. RevPAR in upper upscale fell 13.5%, which was the largest decline in 2024, the result of both declining ADR (-6.2%) and occupancy (-5.9 percentage points). Luxury followed with RevPAR falling 10.4% and upscale posting a 7.3% decline. Midscale chains saw the smallest RevPAR decrease (-1.2%) followed by economy hotels (-2.8%) and upper midscale (-3.6%).

The top 25 U.S. hotel markets saw a larger performance decline than the rest of the country. ADR fell 7% and occupancy dropped 4.1 percentage points, resulting in a 12.2% RevPAR decrease. In addition to Las Vegas, other top markets seeing RevPAR declines of 20% or more included Chicago, Miami and Dallas. Tampa, Houston, Seattle and Detroit were the only markets to post RevPAR gains.

Tampa saw increased hotel demand post-Hurricane Helene, likely associated with recovery efforts. Further impact can be expected in next week’s data due to Hurricane Milton.

Group demand activity lifted Seattle and Detroit, while Houston continued its strong performance due to a variety of factors. Markets outside the top 25 saw RevPAR decline 3.8%.

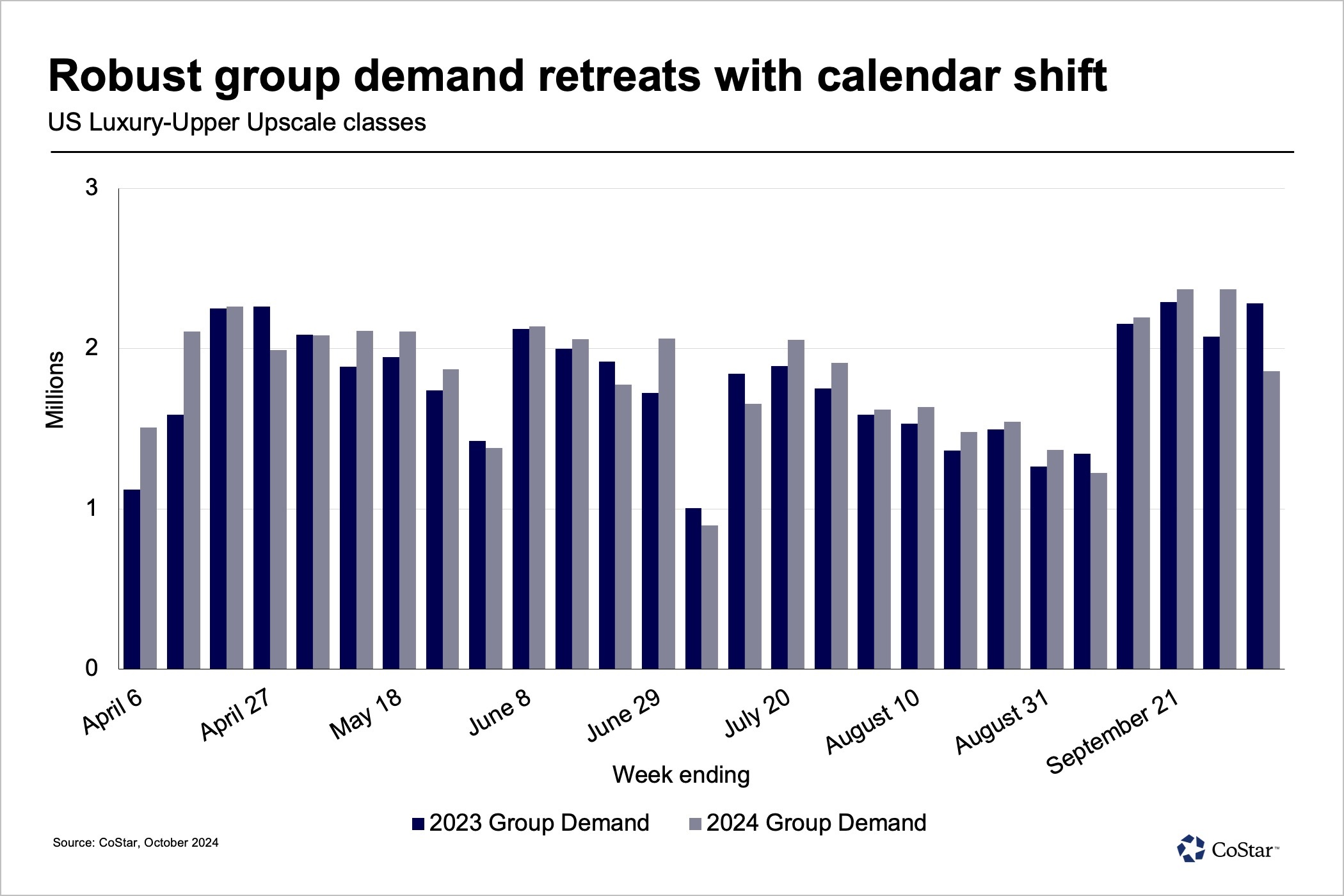

After posting a record demand increase the previous week, group demand in luxury and upper-upscale hotels dropped 18.3%, while transient demand increased slightly (+0.9%). ADR revealed a different pattern with group ADR down 1.8% and transient ADR decreasing 7.9%.

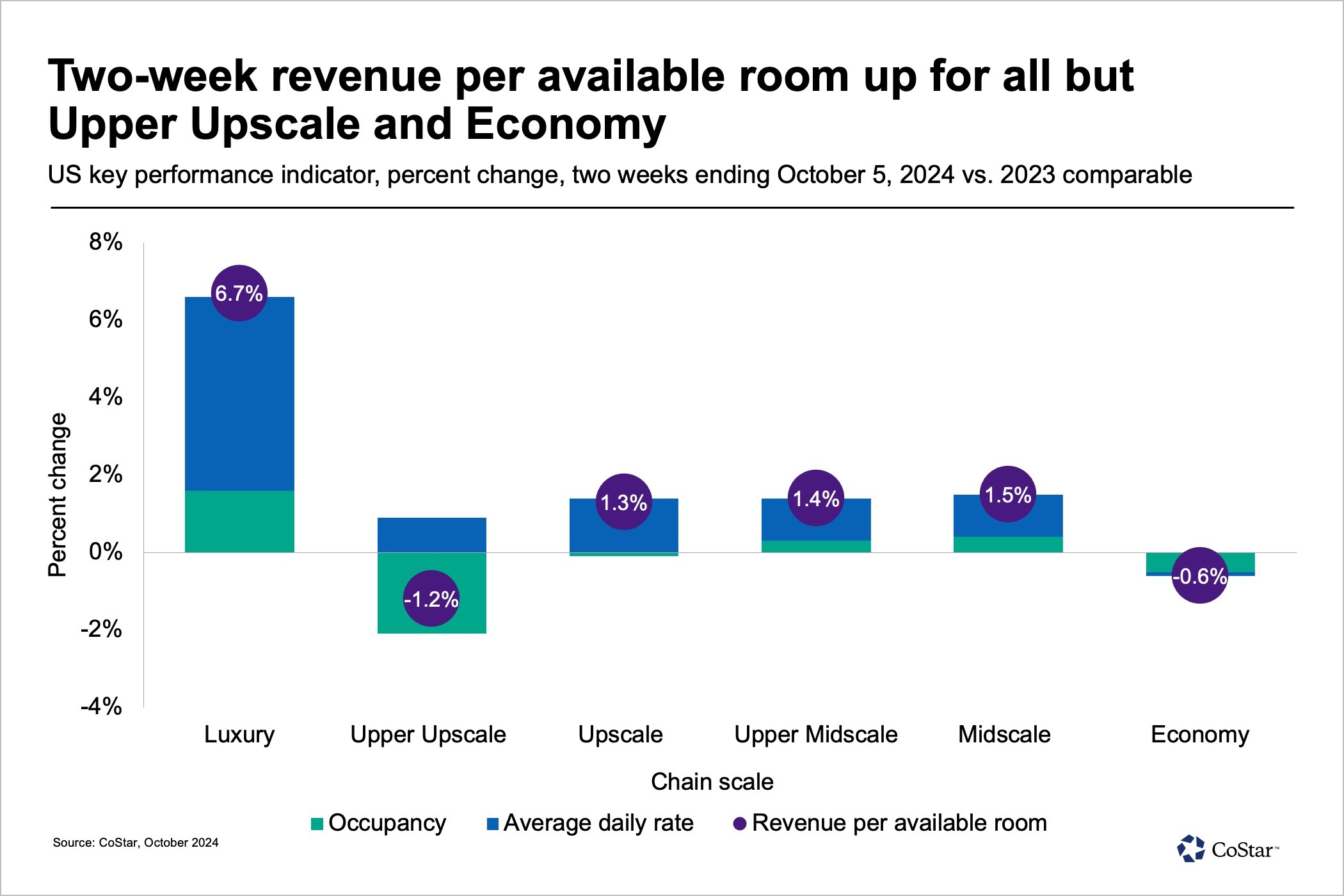

More balanced performance over the past two weeks

Combining the past two weeks to account for calendar shifts, RevPAR increased 1.2%, driven entirely by ADR (+1.5%) while occupancy was essentially flat, down 0.3 percentage points. For the top 25 markets, RevPAR was up 2.2% with the rest of the country gaining a modest 0.5%. RevPAR increased in four chain scales: luxury, upscale, upper midscale and midscale. Comparisons in the upper-upscale and economy segments were down 1.2% and 0.6%, respectively, driven almost entirely by occupancy declines.

Looking ahead

The week ending Oct. 12 should show improvement based on STR’s Forward STAR data even though Yom Kippur occurs at the end of that week; however, the impact of Hurricane Milton may soften this. Markets affected by both Hurricane Helene and Hurricane Milton will be monitored as recovery efforts take place. The remainder of October looks positive up until the week of Halloween, which occurs on Thursday this year.

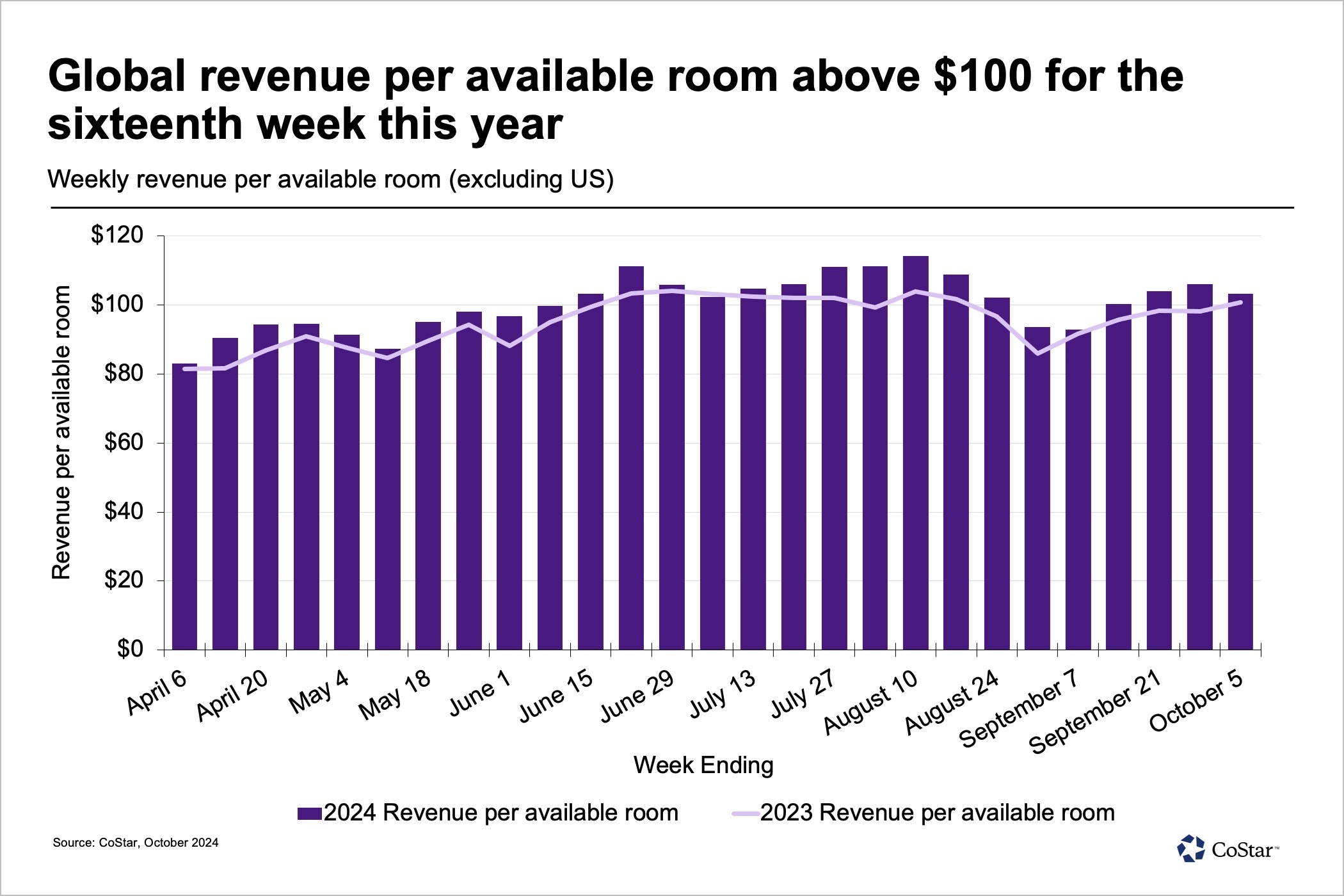

Global hotel RevPAR exceeded $100 for the 16th week this year

During the first week of October, global hotel occupancy rose 1.3 percentage points to 71.2%. ADR growth was more modest, increasing 0.4%. Overall, RevPAR climbed 2.4% to $103, marking the 16th week this year that RevPAR has exceeded $100. However, excluding China, global hotel occupancy fell 1.3 percentage points while ADR increased 4.2%. China’s hotels felt an impact from the Golden Week holidays, which drove occupancy up 8.8 percentage points but caused an 8.9% ADR decline.

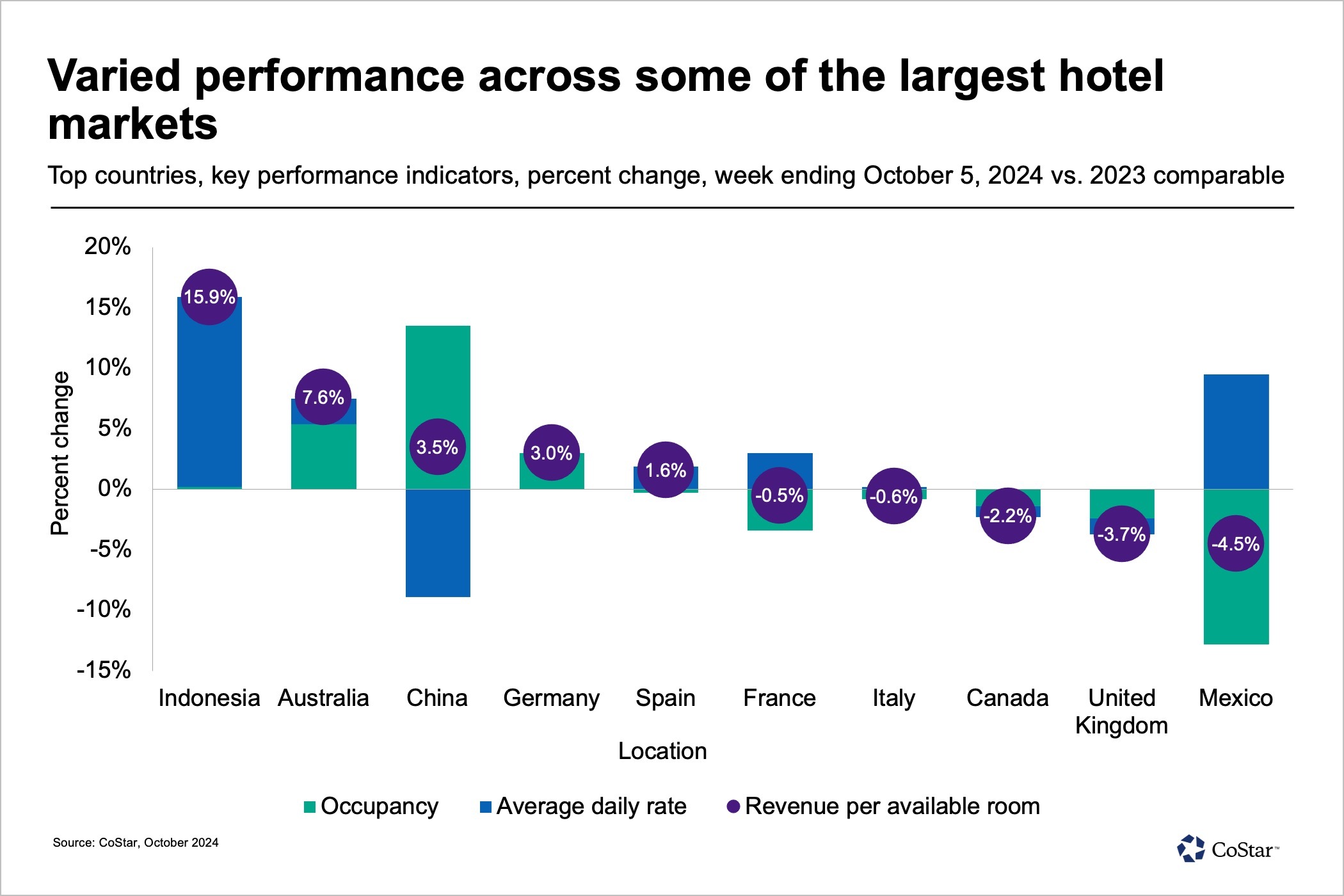

Aligned with spring school holidays, Australia’s hotel RevPAR jumped 7.6% on a 3.9- percentage-point rise in occupancy with ADR up 2.1%. Occupancy gains were recorded in all but one market, Melbourne, where occupancy dipped 1.6 percentage points. Brisbane led the way with a 13.5- percentage-point occupancy increase, followed by ACT & Canberra, up 10.3 percentage points.

Indonesia continued to see strong growth, with performance driven entirely by ADR, up 15.7%. Key market ADR drivers included Central Java (+26%) and Bali (21.6%), benefiting from robust international demand alongside a boost from corporate and government business.

Recent storms and hurricanes have significantly affected hotel performance throughout Mexico, leading to noticeable declines in occupancy across various markets.

Global hotel performance is expected to remain positive throughout the month of October. China performance is starting to turn positive, possibly affected by the recently released economic stimulus plan.

Isaac Collazo is vice president of analytics at STR. Chris Klauda is senior director of market insights at STR. William Anns is a research analyst at STR.

This article represents an interpretation of data collected by CoStar's hospitality analytics firm, STR. Please feel free to contact an editor with any questions or concerns. For more analysis of STR data, visit the data insights blog on STR.com.