With their pragmatic, no-frills rooms attracting travelers from across the spectrum, extended stay hotels have enjoyed an advantage over other hospitality types in this recovery.

Last year, extended stay chains ran at an average occupancy of 73%, as other business-oriented hotels recovered much slower. Given reaccelerating business demand and continued strong leisure travel, expectations are that extended stay hotels will continue to outperform, with further occupancy and rate acceleration and continued strong investor demand.

The recent outperformance has already attracted deep-pocketed investors eager to capitalize on a property type that seems almost recession-resistant. Last summer, Blackstone and Starwood Capital teamed up to take the Extended Stay America chain private at a share price of $20.50 for a total transaction price of about $6 billion, or just under $100,000 per key. And earlier this year, the companies teamed up again to buy 111 WoodSpring Suites hotels for $1.5 billion from Brookfield Asset Management. The WoodSpring Suites brand is owned by Choice Hotels. Wyndham Hotels & Resorts, meanwhile, announced during its fourth-quarter earnings call that it will start a new extended economy brand to add to its stable of companies.

Traditionally targeting guests who often stay for weeks at a time, extended stay properties offer larger accommodations and often full-kitchen areas. Traditional customers include consultants on assignment, construction crews and residents in between living arrangements. At the onset of the pandemic, this accommodation type was also in high demand by traveling nurses and people who needed to quarantine from their families. In addition, throughout the pandemic, workers on longer-term assignments have frequented these hotels.

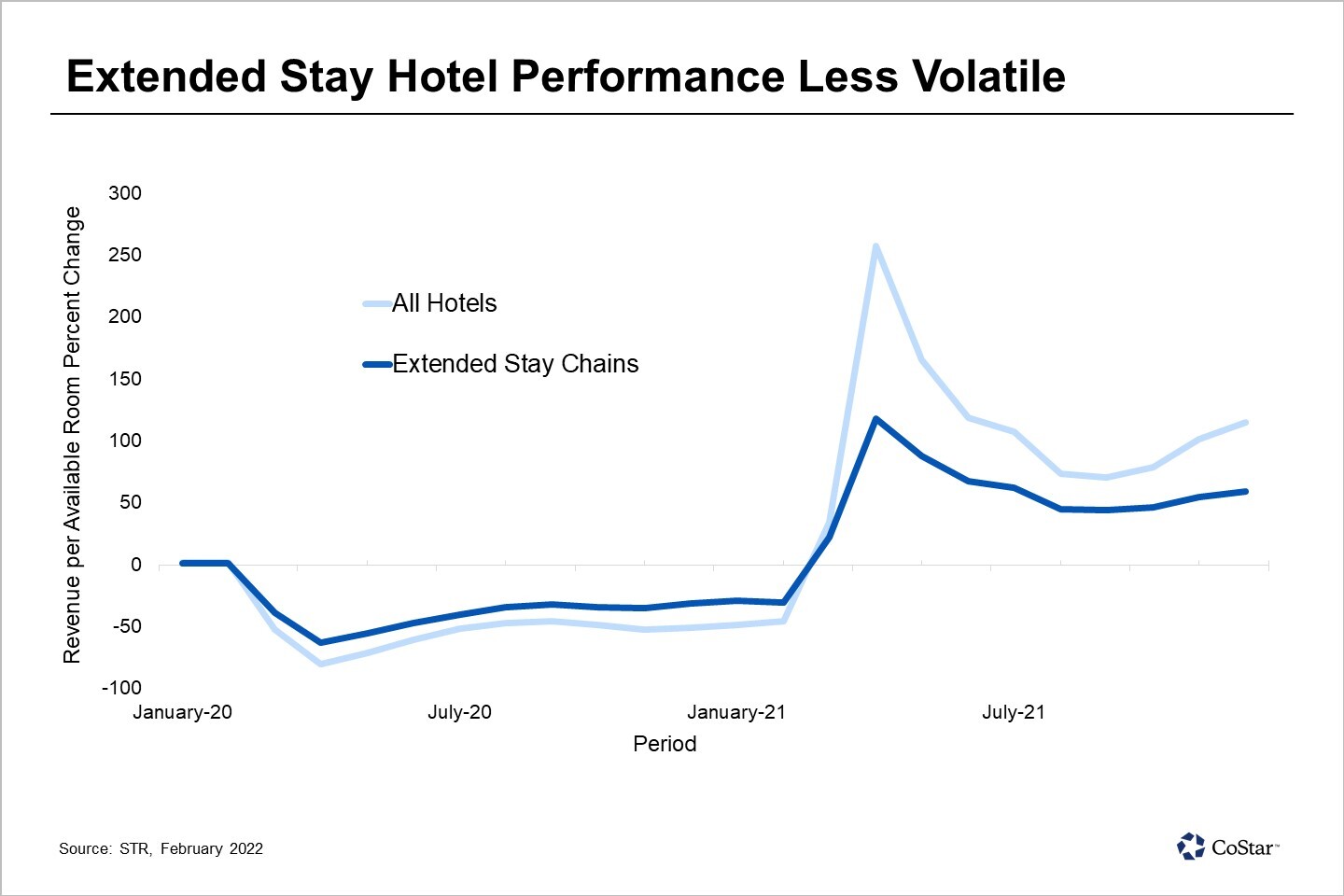

This combination of demand drivers insulated the performance of extended stay hotels from the steep losses suffered by other hotels. The average occupancy for extended stay properties in 2020 was around 60%, roughly 16 points above the U.S. average. Even as the health crisis hit the U.S. and hotel occupancy plummeted to a national average of 24% in April 2020, extended stay hotels maintained a 44% occupancy.

The lower occupancy volatility has meant that changes in revenue per available room, or RevPAR, have been more muted during the recovery. Whereas U.S. hotels in general saw lower room rates and occupancy, extended stay hotels were able to maintain better occupancy but still recorded room rate declines. In the ongoing recovery, the RevPAR increase for extended stay hotels is not as pronounced, precisely because the drop in occupancy was not as steep as it was for all other hotels.

As business travelers begin traveling again in larger numbers, the strong demand and already-high occupancy levels should give extended stay hotels pricing power and allow them to easily surpass their 2019 room rates.

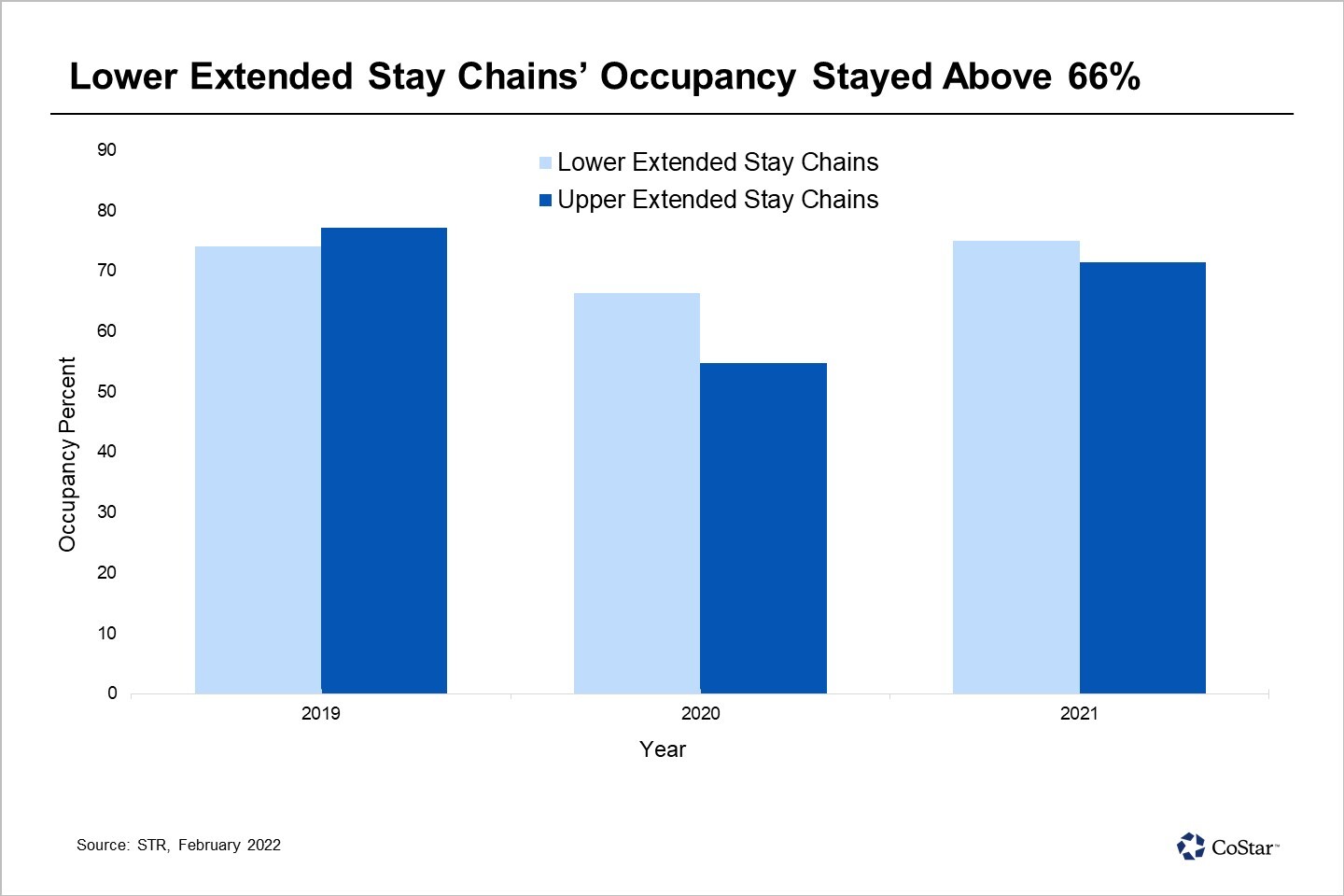

CoStar has two categories for analyzing the performance of extended stay hotels: upper and lower, primarily related to average room rate. Lower-cost extended stay hotels had a 2021 average room rate of $71, while upper chains had an average rate of $125. In 2019, higher-rated hotels also reported higher occupancy, achieving an average of 77% for the full year. This can likely be attributed to the strong economy and related business travel activity from consultants and personnel who had to relocate for weeks or months at a time.

In 2021, the lower-end extended stay hotels achieved an average occupancy of 66%. The occupancy drop between 2020 and 2019 was 10%, much more favorable than the occupancy for all U.S. hotels, which declined by 33%. The strong performance at the lower end points to more demand from independent travelers who chose the accommodation type because of their circumstances, be it for quarantine, to be closer to loved ones or because they relocated to a new city and waited for a more-permanent living situation.

With Blackstone and Starwood becoming major investors in the space, there has been some speculation in the industry on the prospects for converting hotels into apartments. As multifamily capitalization rates continue to compress, higher hotel capitalization rates point to a possible arbitrage opportunity, which could be realized if hotel properties are converted. While no announcements about large-scale conversions have been made, the opportunity is increasingly on investors' minds as 2022 gets underway.