U.S. hotels experienced a down performance week as expected due to spring holidays.

In the week of April 13-19, 2025, U.S. hotel revenue per available room (RevPAR) fell 9.3%, with occupancy declining 5.4 percentage points and average daily rate (ADR) dropping 1.3%. The decrease was expected given that Passover began on the evening of Saturday, April 12 as well as Holy Week, the seven days before Easter on Sunday, April 20. This resulted in lower travel demand along with a difficult comparison to last year given that Easter was in March and Passover was later in the month.

Holy Week performance generally in line with similar weeks

The RevPAR decline this Holy Week was larger than the 10-year average ending in 2019 (-9.3% vs. -3.5%). However, when compared to 2019 alone, the decline was in line. Last year, the measure was down 6% in the comparable week.

Hotel demand was down 7.5% year over year, but compared to Holy Week 2024, the decrease was much less (-0.4%). Additionally, room demand was above the 10-year average and higher than in 2023.

At a property level, on average, hotels in the U.S. sold 1.5 less rooms this Holy Week than last year. By day of week and compared to Holy Week 2024, shoulder days Sunday and Thursday saw the largest demand decreases (-2%) with weekdays Monday to Wednesday flat and the weekend up 0.5%. ADR was basically flat from last Holy Week at 0.2%.

Later Easter helped drive demand in Mid-Atlantic markets

The year-over-year RevPAR declines were similar across the top 25 U.S. hotel markets and the remaining markets with the top 25 seeing a slightly larger ADR decrease. On a Holy Week comparison basis, the top 25 markets saw hotel demand go backwards (-2.3%) from a year ago, whereas all remaining markets saw it go up 0.8%.

The markets seeing strong growth included Myrtle Beach, Norfolk/Virginia Beach and the New Jersey Shore. The later Easter, with its warmer weather, likely helped drive stronger demand to those markets. Additionally, 28% of all K-12 students were on spring break last week versus only 3% in the year before.

Among the top 25 markets, Las Vegas accounted for much of the demand loss from Holy Week a year ago. Other markets losing demand included Atlanta, Nashville and Washington, D.C. Those seeing stronger, comparable Holy Week metrics included Boston, New York City and Philadelphia.

Given the large number of students on spring break, it was not surprising to see TSA screenings up 0.6% for the week, the second straight week of gains. As of April 19, month-to-date screenings were down 0.8%, but April year to date was up 0.5%.

Canadian and Mexican border hotels followed total US hotel industry

U.S. hotels near a Canadian border crossing saw demand fall 9.8% year over year with those near a Mexican border crossing dropping 1%. Compared to Holy Week 2024, demand was up in Canadian border hotels (+1.3%) but falling for those near Mexican ones (-4.9%). ADR and RevPAR on this comparison basis were down across all border hotels.

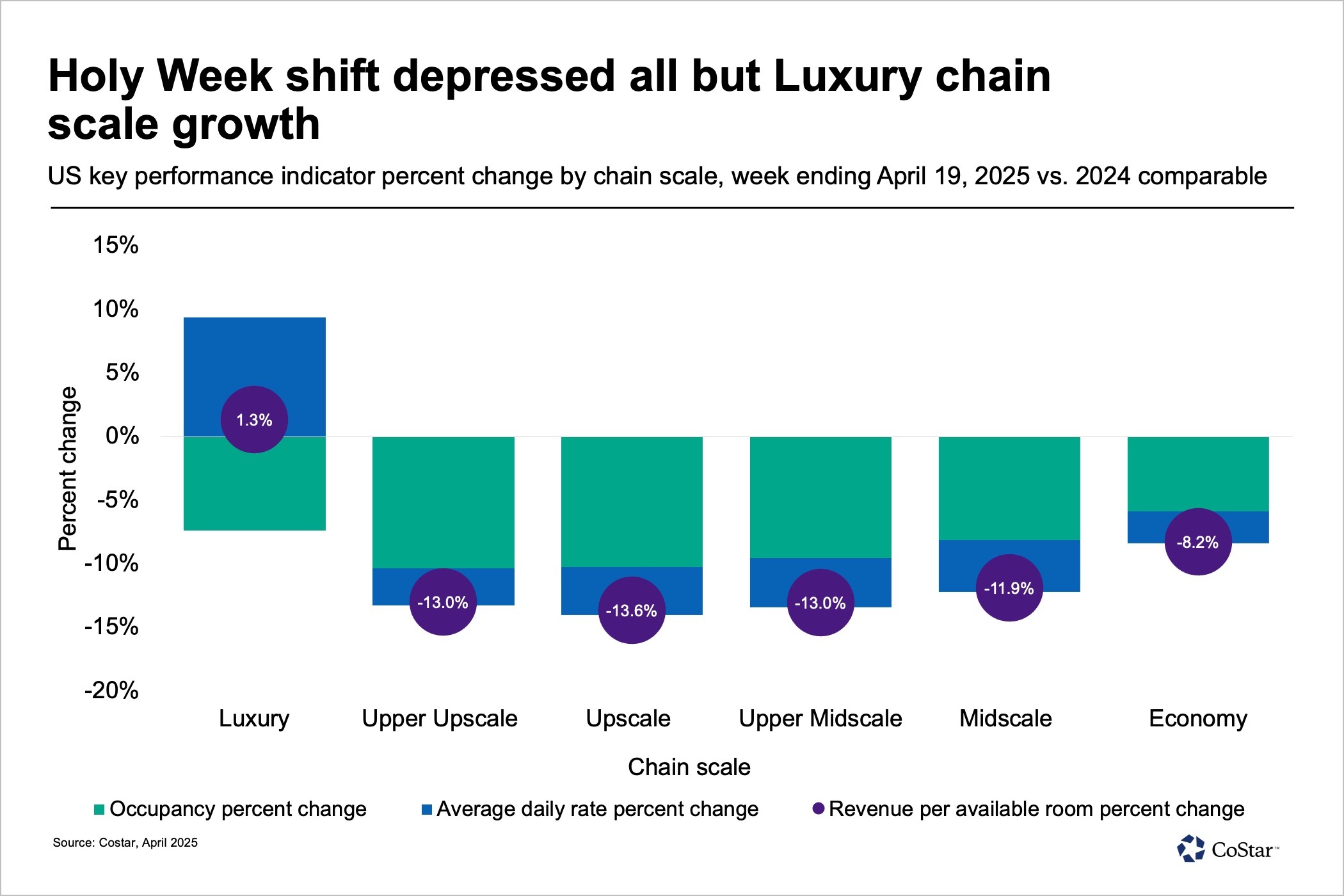

Holy Week shift responsible for declines across chains scales and group travel

Except for luxury hotels where RevPAR rose 1.3%, all other chain scales posted RevPAR declines due more to occupancy than ADR. RevPAR declines ranged in the low double-digits for all but economy, which decreased 8.2%.

Not surprising, group demand in luxury and upper-upscale hotels retreated, down 40.1%, while transient demand increased 11.5%. Holy Week in 2019 experienced similar shifts with group demand falling 33.1% and transient demand rising 14%.

Looking ahead

This week’s slowdown was expected, and the week of April 20-26 should improve week over week but remain below last year’s levels due to Easter Sunday. The rest of the week will benefit from an easy comp to Passover week, which occurred last year from 22-30 April. More normal trading conditions, free of holiday shifts, are expected the following week while we will continue to monitor economic, political and consumer trends as they relate to travel across the globe. A cleaner calendar will make impacts from those factors far clearer.

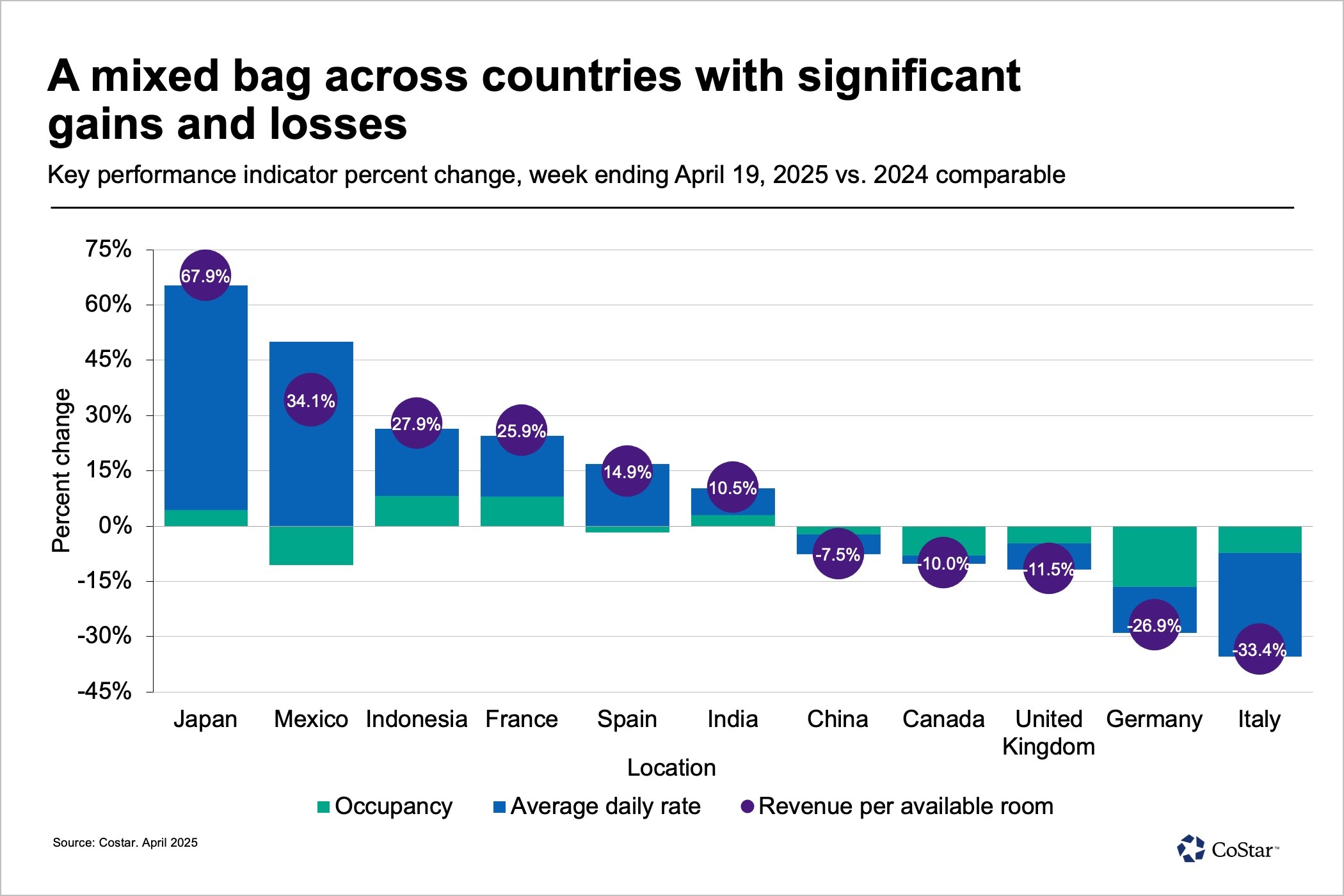

Global hotel performance a mixed bag

Hotel RevPAR across the globe increased by double-digits for a third consecutive week, rising 10% entirely on ADR (+11.4%) while occupancy declined (-1 percentage points). Japan, hosting EXPO, led the charge (+67.9%), and was followed by Mexico (+50%), which is in peak spring season. Also topping the list were Indonesia (+37.9%) with 10 of 12 markets seeing RevPAR gains and France (+25.9%) with 9 of 12 markets recording increases, including Paris hosting the Paris Marathon.

On the flip side, Italy, Germany, the United Kingdom and Canada all posted double-digit declines due to event calendar shifts and the Holy Week slowdown. China also saw RevPAR decrease 7.5% on a combination of ADR and occupancy declines. RevPAR had declined in China in 15 of the past 16 weeks, mostly on falling ADR.

Isaac Collazo is senior director of analytics at STR. Chris Klauda is director of market insights at STR.

This article represents an interpretation of data collected by CoStar's hospitality analytics firm, STR. Please feel free to contact an editor with any questions or concerns. For more analysis of STR data, visit the data insights blog on STR.com.