Given the comparison to Easter week last year, U.S. hotels saw revenue per available room soar 7% during the week of March 23-29 thanks to occupancy growth, which increased 2.8 percentage points, while average daily rate rose 2.5%. Not surprising, weekend RevPAR was up the most (18.5%) with occupancy rising 8.9 percentage points and ADR up 4%. RevPAR during the weekdays from Monday to Wednesday increased 2.9%, primarily due to ADR growth of 2.4%. RevPAR on shoulder days Sunday and Thursday increased a modest 0.9% driven equally by ADR and occupancy.

While U.S. hotel ADR growth was better this week than in the previous one, it continued to lag inflation. March month-to-date ADR is up 1.4%, which is 1.2 percentage points less than our inflation expectation. A lag is also evident quarter-to-date but to a slightly lesser extent.

Basketball, hockey and baseball lifted hotel performance across host markets

The two strongest top 25 U.S. hotel markets were smaller ones: St. Louis & Minneapolis. St. Louis earned the top honor by hosting the World of Asphalt Show & Conference. Hotel occupancy rose 16.3 percentage points and ADR increased 15.8%, resulting in a 47% RevPAR gain. St. Louis also hosted the Cardinals Opening Day baseball game. Minneapolis took second place with RevPAR increasing 28.8% driven by strong group and transient demand. Its weekly occupancy increased 10.4 percentage points with ADR up 5.8%. Fourteen of the top 25 markets saw RevPAR growth of more than 7%.

Across the next 25 largest hotel markets, Louisville, Kentucky, was on top, driven by the KHSAA Boys’ Sweet 16 State Basketball Tournament, which was held a week earlier last year. RevPAR rose 64.8%, which more than made up for the 36.1% decline seen last week. Amateur basketball also drove Richmond, Virginia, where hotel RevPAR increased 38.2% via the Big Shots Virginia Showtime tournament. NHL hockey benefited Columbus, Ohio, with RevPAR advancing 31.3%.

Markets hosting the NCAA’s basketball tournament games varied depending on their size. The smaller markets generally saw the largest impact. On the men’s side, weekend RevPAR ranged from up 64.4% in Indianapolis to up 11.9% in Newark, New Jersey. Hotel RevPAR in Atlanta and San Francisco, the other two cities hosting the regional finals, rose 34.5% and 22.7%, respectively. The two markets hosting the women’s games – Birmingham, Alabama, and Spokane, Washington – saw weekend RevPAR rise 47.3% and 28.9%, respectively.

Overall, 57% of all U.S. markets saw weekly RevPAR growth above the national average.

Luxury hotels took a backseat this week

Upper-upscale hotels saw the largest RevPAR gain, up 10.1% with the next three chain scales – upscale, upper midscale and midscale – close behind ranging from 9.1% to 8%. Luxury hotels saw RevPAR increase 4.9%, which was nearly the same as seen in economy hotels. Occupancy played a more significant role in driving RevPAR across all chain scales with the middle four chains scales recording occupancy gains averaging 3.7 percentage points. Luxury and economy hotel RevPAR was also lifted more by occupancy but to a lesser degree. The middle four chain scales also saw stronger ADR growth – between 3% and 4% – as luxury ADR increased 2.1% and economy ADR increased 1.6%.

Group demand had the most to gain from the easy comp

Group demand in luxury and upper-upscale hotels skyrocketed 40.8% with ADR up 11.8%, propelled by the easy comparison to last year. Group travel felt a major impact from the calendar shift. Markets across the country saw increased demand with 23 of the top 25 markets seeing positive gains. St. Louis, Nashville, Philadelphia, Orlando, and Minneapolis all posted more than 10-percentage-point gains in occupancy. Markets outside the top 25 also experienced strong group demand growth. Nationally, transient demand declined 4.8% with ADR up a modest 1% with both top 25 markets and all others seeing transient decreases.

Hotel demand in border towns remained mixed

Demand across 1,306 hotels within 50 miles of the Canadian border increased for the second consecutive week, up 5.4%. On the Mexican border – which includes 916 hotels within 50 miles of the southern border – demand decreased 4% following an increase a week ago. Keep in mind that national hotel room demand was up 5.1%. Occupancy in hotels near U.S.-Mexico crossings were still running health occupancy (66.5%) versus those near Canadian borders (51.8%). Over the past 28 days, U.S. demand increased 0.7% whereas demand on the Canadian border is flat (+0.2%) and down 1.7% on the Mexican border.

Hurricane markets and Los Angeles submarkets elevated

For the first time, hurricane markets matched U.S. performance. The Easter shift makes it difficult to decide whether performance is due to continued hurricane recovery or spring break. One market that has consistently posted stronger performance is Augusta, Georgia, which continues to experience the greatest impact of all 13 markets tracked with RevPAR up 36.7% this week. The Masters tournament takes place April 10-13 and part of this lift may be due to activity in advance of the tournament.

Two of the three submarkets most affected by January’s wildfires in Los Angeles continued to see elevated RevPAR: Los Angeles East (+28.4%) and Pasadena/Glendale/Burbank (+21.6%). Los Angeles North, which had seen elevated albeit more modest increases, came down this week with RevPAR up just 1.7%.

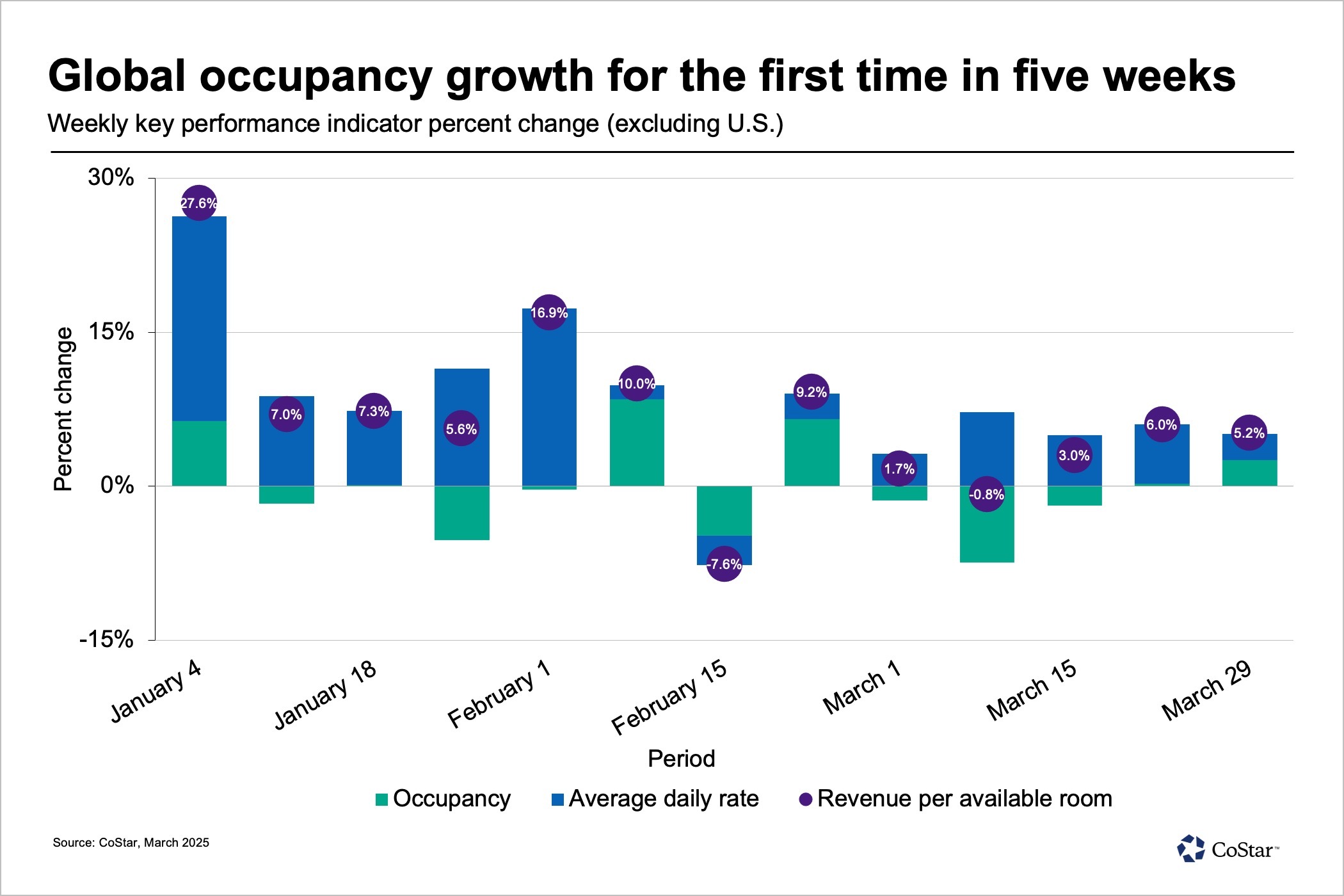

Global performance also benefited from the easy comp

Globally, hotel occupancy increased 1.7 percentage points to 67.5%, which was the first significant increase in six weeks, but mostly due to the easy comp. ADR rose 2.5%, continuing its growth streak – up in 59 of the past 61 weeks – resulting in a RevPAR gain of 5.2%.

Among the top countries based on hotel supply, Germany had the largest RevPAR increased – up 46.4% – due to conferences and fairs taking place this week unlike last year when these events shifted away from Easter week. Occupancy (+14.9 percentage points) drove the RevPAR increase with ADR growing 15.7%. Among other large countries:

- RevPAR in India advanced 23.4% and was also driven by occupancy (+8.9 percentage points) as ADR increased 7.7%.

- Mexico’s RevPAR (17.6%) continued to driven by ADR (8.9%) but to a lesser extent than in previous weeks. For most of the year, ADR in the country has been rising by more than 20%.

- Japan’s RevPAR continued to expand (4.8%) on ADR with occupancy declining. Occupancy has declined for the past four weeks with this week’s decrease (-2.8 percentage points) the largest of the four.

- China experienced a seventh consecutive week of falling RevPAR (-2.8%) albeit the lowest decline of the past four weeks.

- Indonesia posted the largest RevPAR decline of the large markets due in part to the end of Ramadan and the celebration of Eid al-Fitr on March 29.

Looking ahead

In the week ending April 5, we expect U.S. and global RevPAR to advance again due to a second week of easy comparisons due to the Easter shift. For the U.S., the week ending April 12, is questionable due to headwinds from last year’s solar eclipse on April 8, 2024. STR’s Forward STAR is showing occupancy on the books up 1.5 percentage points for top markets. However, last year’s event was also spread out across many smaller markets, which will not see the same level of occupancy this year as the top markets are expected to have. Thus, our back-of-the-envelope forecast has demand flat for that week. Easter week is in the week of April 19 with demand and RevPAR falling across the globe. Easter will also affect the week ending April 26.

Isaac Collazo is senior director of analytics at STR. Chris Klauda is senior director of market insights at STR.

This article represents an interpretation of data collected by CoStar's hospitality analytics firm, STR. Please feel free to contact an editor with any questions or concerns. For more analysis of STR data, visit the data insights blog on STR.com.