It’s the summer of the leisure traveler and while hotel occupancy remains below 2019 levels, average daily rate has surpassed its pre-pandemic levels in recent weeks as hoteliers take full advantage of pent-up demand.

However, even as summer provides much-needed relief to the industry, operators remain wary of the post-Labor Day hospitality landscape.

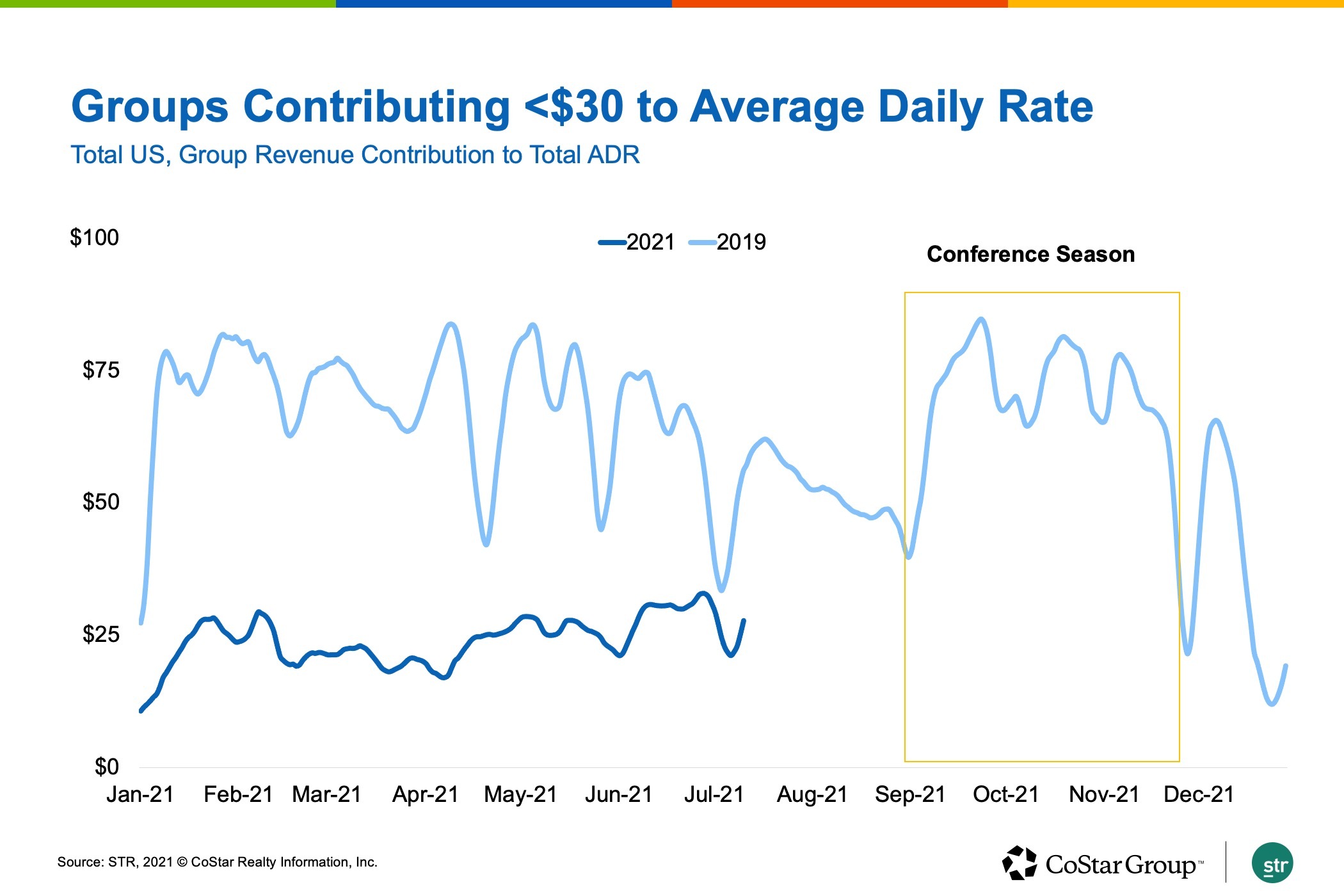

Transient demand has nearly returned to pre-COVID-19 levels, but group demand remains well below comparable 2019 figures, which is an increasing concern as the fall conference season approaches.

Prior to the pandemic, groups contributed about $50 to rates over the summer months, a figure that jumped about $20 from September through November.

At the same time, transient occupancy fell around eight points from its summer highs of just over 50% and group occupancy crept up from 20% to around 25%. Given that transient travel patterns have closely mirrored 2019 trends this summer, it’s likely that transient leisure demand will slacken after Labor Day.

This spells concern for the industry, as the groups that normally replace leisure travel over the transitory fall months aren’t expected to return in significant numbers until early 2022. Groups currently contribute less than $30 to luxury and upper upscale hotel ADR, which came in at $235 for the week ending July 10, a staggering $24 increase over 2019.

Transient revenue accounted for the increase in ADR, as group and contract revenue both declined considerably compared to the same week in 2019. With group demand at less than half of its 2019 level, that trend is unlikely to change soon.

As a result, short-term summer rates are likely to remain high, but as the seasons change and leisure travelers head home, both demand and ADR recovery may stall. While headline figures may appear “normal,” segmentation reveals the weak spaces in hospitality recovery and can help operators identify the sources of demand necessary to fully recover.

Kelsey Fenerty is a research analyst at STR.

This article represents an interpretation of data collected by STR, CoStar's hospitality analytics firm. Please feel free to contact an editor with any questions or concerns.