The U.S. hotel industry sold the most hotel room nights since late October, as the latest weekly performance data shows that while geopolitical tensions around the Russian invasion of Ukraine have elevated gas prices, there has been no noticeable effect on hotel demand.

As of last week, U.S. gas prices were up $0.98 per gallon year over year. For a typical car with a 12-gallon tank, the increase per week is under $12, which equates to a yearly impact of $624.

Hotel occupancy and demand, meanwhile, continue to rise weekly. Total U.S. hotel occupancy for the week ending Feb. 26 was 62.6%, up from 59.1% the previous week, as the industry sold 23.9 million hotel room nights.

Weekend hotel occupancy was 70.6%, down from 73.7% the previous weekend, which included the Presidents Day holiday. But for the weekdays — Sunday through Thursday — hotel occupancy increased by more than five percentage points week over week, from 53.2% to 58.8%.

While there is no doubt that weekday occupancy was supported by the Presidents Day holiday — Sunday and Monday — that’s not the full story as occupancy was even stronger Tuesday through Thursday at 61%.

The weekday occupancy increase also indicates continued recovery in business transient and group travel demand.

Further backing that up, the U.S. top 25 markets together averaged 65% occupancy for the week — the first time since early August and only the seventh time that top 25 occupancy has reached that mark since pandemic lockdowns began.

Occupancy during the week surpassed 70% in eight of the top 25 markets, including Los Angeles, San Diego and Miami. Demand in Miami was helped by the South Beach Wine & Food Festival, which attracted 90,000 attendees.

Group demand also reached a 15-week high, and a level that was more than half of what it was in the same week of 2019. In the top 25 markets, group demand is now 55% of what it was in 2019, up from 50% two weeks ago. Among luxury and upper-upscale hotels in the top 25 markets, group demand increased to 60% of the 2019 comparable. Weekday group demand was lower than what it was in 2019, whereas weekend group demand was higher. Overall, occupancy for upper-upscale hotels reached 61%, which was the highest such level since summer 2021.

U.S. hotel industry average daily rate advanced 2.2% week over week to $144, marking the seventh-straight week-over-week increase and the second-highest level ever after Christmas week 2021.

Weekday ADR was up 7.4%, while weekend ADR declined 4.9% in comparison with the holiday weekend. The number of hotels with ADR above $1,000 continues to increase, with 95 hotels in that category, the third-largest number of hotels with that level of ADR since 2019.

Revenue per available room increased 7.6% to $89.45, which was the best level since late August.

U.S. RevPAR has also increased for the past seven weeks — the longest streak since summer 2021. Industrywide RevPAR surpassed the 2019 comparable by 8%. This was only the sixth time since the start of the pandemic that weekly RevPAR beat the comparable week from 2019.

Absolute RevPAR remained the highest over the weekend in the top 25 markets, where it topped $126. But like with ADR, weekend RevPAR was down from the previous weekend, dropping by more than 8% in the top 25.

On a market level, 61% were at “peak” RevPAR, exceeding the comparable week of 2019. On an inflation-adjusted basis, 51% of markets were at “peak” RevPAR. The 28-day moving average shows 49% of markets with RevPAR above the 2019 comparable, but 19 markets remained in either “recession,” with RevPAR between 50% and 80% of the 2019 comparable; or “depression,” with RevPAR less than 50% of what it was in 2019.

Market Highlights

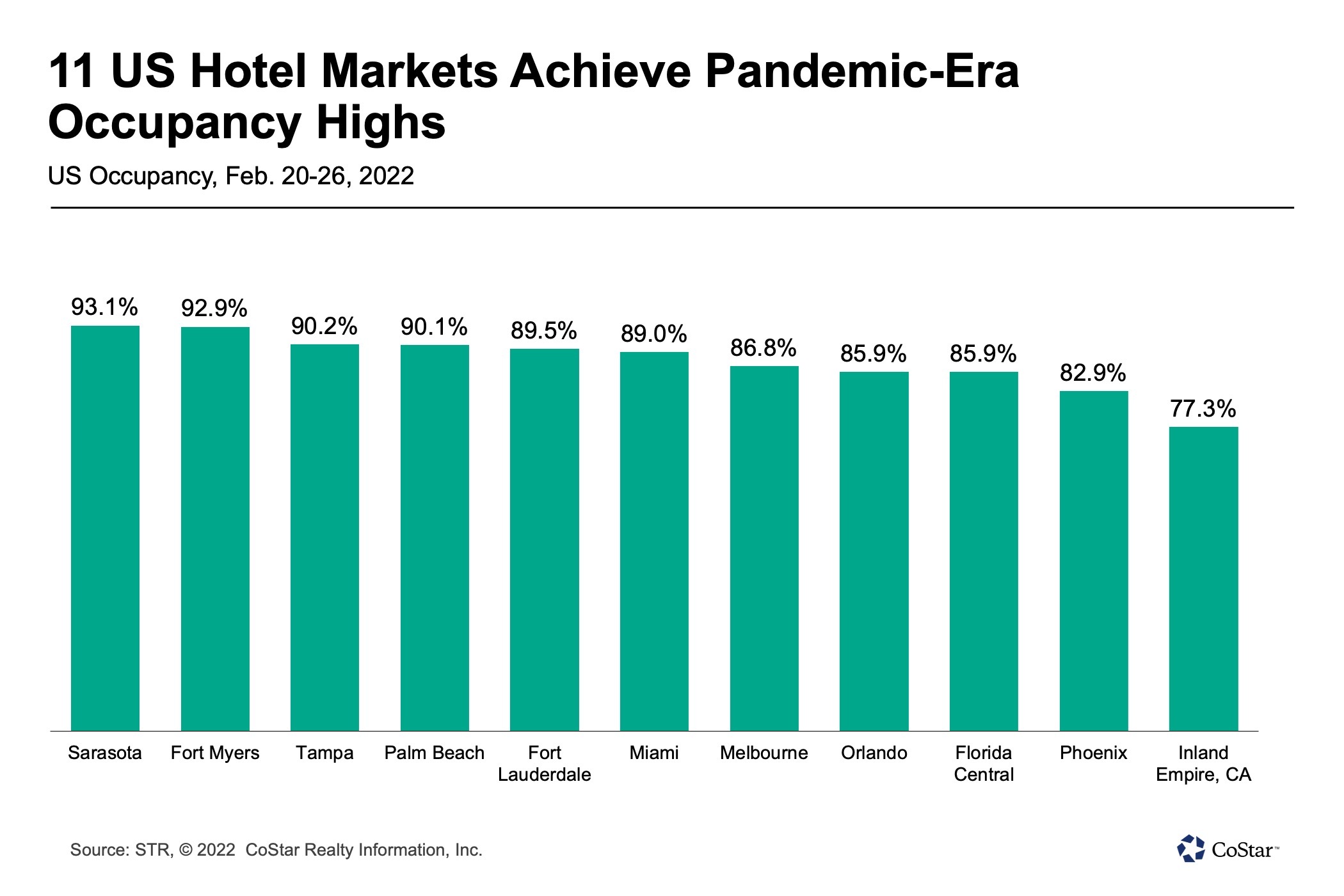

Eleven STR-defined markets, nine of which were in Florida, reached weekly pandemic-era occupancy highs.

Orlando, the nation’s second-largest market based on supply, posted hotel occupancy of 85.9%, marking only the 11th time that Orlando has surpassed 85% occupancy in the past 165 weeks and the market’s highest occupancy since the week ending Feb. 22, 2020.

The two non-Florida markets that reached pandemic-era highs were Phoenix and Inland Empire, California, which includes the cities of Palm Springs, Palm Desert, Ontario and others east of Los Angeles.

The highest weekly occupancy was again reported in the Florida Keys at 94%, followed by Sarasota at 93%, Fort Myers at 93%, and Tampa and Palm Beach, both at 90%.

In total, 15 markets reported occupancy above 80%, up from eight the week before. Another 17 markets reported occupancy between 70% and 80%. Occupancy increased week over week in 85% of markets.

San Francisco hotel occupancy remained above 53% for a second consecutive week while Washington, D.C., also neared that level. New York City reached 61%.

Markets categorized as central business districts also advanced with occupancy of 57%, up more than two points from the previous week. The Houston central business district showed the largest week-over-week gain as occupancy was up 18 percentage points, supported in part by the annual Houston Livestock Show and Rodeo, which will continue through March 20. The Chicago and Tampa central business districts followed with nearly eight percentage points of occupancy growth. Occupancy for hotels in urban locations increased to 58% with those in the top 25 markets rising to 57% occupancy.

Eighty percent of the 166 STR-defined markets reported higher ADR this week versus the comparable week of 2019. Adjusting for inflation, 48% of markets surpassed 2019 ADR levels, which was the highest weekly percentage since the Christmas holiday.

ADR growth was the strongest among hotels in small metros and towns, up 4.6%, and at resorts, where rates were 3.8% higher. Hotels in suburban, airport and urban locations reported declines in weekly ADR of 0.5%, 0.6% and 1.5%, respectively.

ADR growth was also weaker in the top 25 markets, where it was up only 0.5%, mostly because of an 18% week-over-week decrease in Los Angeles post-Super Bowl. Excluding Los Angeles, ADR in the top 25 markets increased 2.8%.

Los Angeles was not the only top 25 market to report a week-over-week decrease in ADR, as a similar change occurred in San Francisco, Denver, St. Louis and nine other markets.

Isaac Collazo is VP Analytics at STR.

This article represents an interpretation of data collected by CoStar's hospitality analytics firm, STR. Please feel free to contact an editor with any questions or concerns. For more analysis of STR data, visit the data insights blog on STR.com.