Despite a difficult year for the global hotel industry, performance stands out as bright spots in some markets, while others are notable for glaring historic lows.

As part of the Hotel Data Conference Global Edition, STR's Brad Garner, senior vice president of client services and relationships, and Aoife Roche, commercial director, hotels, shared some key takeaways of U.S. and international hotel performance in markets that both outperformed and underperformed since the start of the COVID-19 pandemic in March 2020. STR is CoStar's hospitality analytics firm.

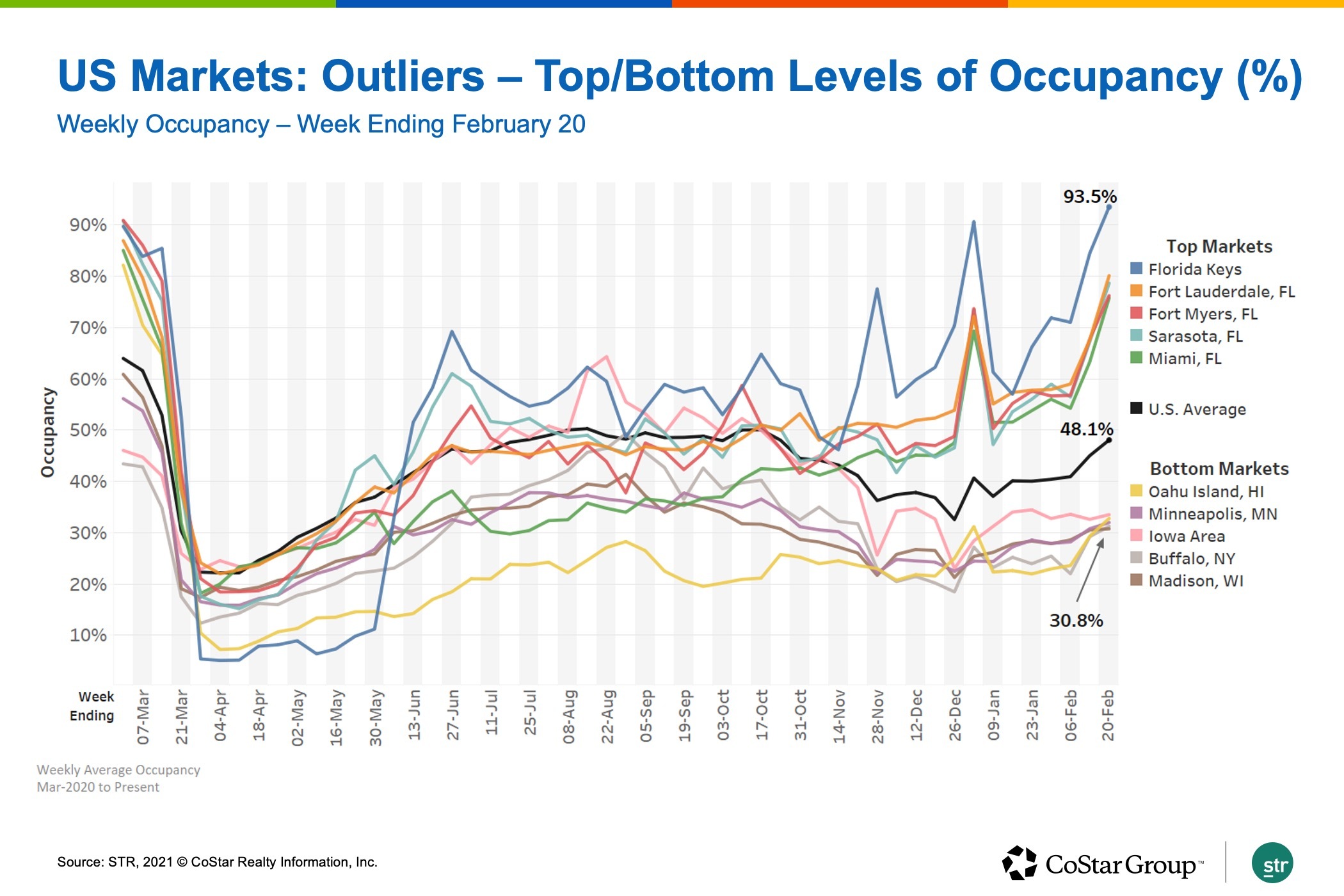

A look at weekly hotel occupancy over the past year shows several Florida markets were among the top markets in the U.S., outpacing the 48.1% nationwide occupancy average, Garner said.

"I think it's no surprise seeing some of the Florida markets there, and what's driving that is certainly leisure demand, warmer climates and people traveling for those types of amenities that Florida has to offer," he said.

In terms of weekly average daily rate, Maui hotels led the way during the past year. For the week ending Feb. 20, they recorded an ADR of $465, much higher than the total U.S. ADR for the same week, which was $102. This is even despite much lower hotel occupancy across the Hawaiian islands since the pandemic started, Garner said.

On the opposite end of the performance spectrum, New York City's hotel market had a tough year. Fewer than half of all hotel rooms in the city were sold during the week ending Feb. 20, and ADR has hovered below $140 since April 2020.

"When you think about New York, it's interesting to see just this bellwether market that typically leads all U.S. markets with performance, whether it be driving room revenue, certainly amongst the highest ADRs and certainly among where — all things being equal — they realize an occupancy greater than 85%," Garner said.

New York's group demand has been "dormant," which puts it in the same boat as San Francisco, he said.

"It's frustrating, bordering on depressing, to see a market like San Francisco struggle," he said. "Same thing, little to no group, which is what absolutely drives San Francisco. I would also offer that California has been a bit more rigid about opening up the market, [enforcing] mask mandates and shutting down."

San Francisco's hotels were just over a third full during the week ending Feb. 20, and ADR was $116, nearly $200 less than a year ago.

"No group demand, leisure demand has been stymied, so the result is really a tremendously weak ADR right now, about $120," Garner said.

International Markets

Outside of the U.S., markets such as Sanya, China; Sochi, Russia; and Dubai, United Arab Emirates, outperformed most other global markets in terms of occupancy and ADR throughout the pandemic year.

Sochi hotels seemed to benefit from a growth in domestic travelers, Roche said.

"Sochi not only outdid all of the Russian markets that we report on, it also outdid all the European markets," she said.

Sochi hotel occupancy spiked in the summer months as COVID-19 restrictions eased and remained above 80% through October, Roche said. After a holiday dip, it's back up in early 2021.

"So really this market is benefiting from staycation business through the summer, and then particularly through Christmas and the New Year, where normally Russians are lured by the Swiss and French Alps, they stayed local," she said.

In the Middle East, Dubai had a notable 2020 as quarantine restrictions were relaxed in the summer, leading to the start of a "solid recovery," Roche said.

During April, May and June, Dubai had strict lockdown restrictions in place, and the borders did remain closed until July 7 when those borders reopened.

"Staycation business boomed, and so did international inbound travel, so that domestic and international leisure travel — and of course, some corporate travel — continues to grow across 2020 and that's peaked in the winter months," she said.

Path to Recovery

There are reasons to be optimistic about small steps toward recovery in 2021, Roche said. It's likely, however, that hotels in markets with strong domestic demand will be the first to ride the wave.

"Demand will absolutely recover, but it will most likely look very different," she said. "In terms of the demand, we expect leisure demand to recover much earlier than corporate demand. So starting in summer 2021, we should start to see some fruits. The domestic demand will of course dominate. ... The accessibility of your destination is very important for your recovery."

In the U.S., some markets have a more favorable demand forecast, Garner said.

"We basically indexed demand at 2019 levels, so this chart supposes that over time, what is your fair share of demand or rate of recovery, compared to 2019," he said.

U.S. markets such as Nashville, Atlanta, Seattle and Dallas could fully recover demand by 2023, but New York, New Orleans, St. Louis and Honolulu might not fully return to 2019 demand levels until 2024 or 2025.

Internationally, hotels in Shanghai, Dubai and Moscow are likely to recover demand by 2023, while markets such as Barcelona, Prague and Bangkok might need to wait until 2024 or 2025, Roche said.

"Markets like Barcelona and Prague — that are hugely dependent on transatlantic business, group business and events business — will have a much slower recovery," she said.