BROOMFIELD, Colorado—Since 2011, STR has looked at the impact the Super Bowl has on the host city from a hotel perspective, both in terms of absolute performance and year-over-year change.

We have been particularly interested to see the impact this year on the Minneapolis/St. Paul market, the third-smallest hotel market of the last eight Super Bowls, and the smallest since New Orleans in 2013. The size of the market, among with other factors, led to high expectations of potential revenue-per-available-room increases on Super Bowl weekend.

This year, we broke the data down by the following locations:

- overall Minneapolis/St. Paul market;

- the submarkets of Bloomington, Minneapolis CBD, Minneapolis North Area, Minneapolis South Area, and St. Paul; and

- the city of Minneapolis.

Occupancy

Unsurprisingly, the Minneapolis CBD submarket, which contains the U.S. Bank Stadium, achieved the highest occupancy at 99% for the Friday, Saturday and Sunday nights of Super Bowl weekend, followed closely by the city of Minneapolis overall. The Bloomington submarket also showed an extraordinarily strong occupancy of 97.2%. The Minneapolis/St. Paul market’s overall occupancy was 92.5% for the weekend, with only two submarkets performing below a 90% occupancy level.

ADR

Average daily rates were significantly boosted throughout the market, with CBD hotels again leading the other submarkets with an ADR of $492, significantly higher than the next highest submarket. ADR trends by submarket closely follow occupancy trends, with Bloomington achieving the second-highest ADR and the Minneapolis South Area showing the lowest ADR.

RevPAR

Every submarket in the Minneapolis/St. Paul area saw incredibly impressive RevPAR increases of over 500% when compared to the same weekend in 2017, with the exception of St. Paul. Hotels in the CBD were again the standout, with an average RevPAR lift of 858%.

Comparison to past years

Comparing this performance to the performance of the seven previous Super Bowl host cities provides context to just how significant the impact was this year in the Minneapolis/St. Paul market.

The following charts examine the comparative impact of all eight host areas, first for the weekend of the Super Bowl itself, and then for the two weeks leading up to the game.

Occupancy – Super Bowl weekend

The Minneapolis/St. Paul market’s strong 92.5% Super Bowl weekend occupancy was the fourth-highest of the past eight years, greatly exceeding the performance of Dallas, New York, San Francisco/San Jose and Houston. This is more than double the market’s occupancy the previous year over the same three days.

ADR – Super Bowl weekend

The $354 ADR reached by Minneapolis/St. Paul hotels was surpassed only by the Super Bowl weekend rates in New Orleans, Phoenix and San Francisco/San Jose. This impressive rate performance helped to boost the market’s RevPAR increase to nearly double the increase seen in recent years.

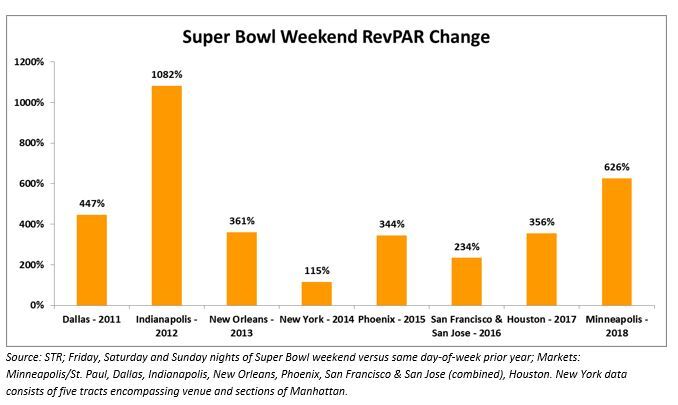

RevPAR percent change – Super Bowl weekend

The RevPAR gains in the Minneapolis/St. Paul market are impressive on their own, but particularly so when compared with gains seen in Super Bowl host cities in the last eight years. The market’s RevPAR lift of 626% was surpassed only by Indianapolis’ astounding increase of over 1,000%.

Minneapolis and Indianapolis both typically see slow performance in early February, giving them the most room to grow in occupancy and rate. More consistently strong performing markets such as New York and San Francisco have higher baselines to use as comparison points, so growth is more muted in those markets.

Another important factor in a market’s ability to produce high RevPAR gains from a special event is the market’s size. Markets with many more rooms to fill can end up limited in their RevPAR gains, while smaller markets tend to demonstrate greater pricing power. Indianapolis and Minneapolis are the prime examples of this, with some of the lowest hotel supply and the largest RevPAR increases.

Super Bowl weekend RevPAR percent change relative to market size

Two weeks leading up to Super Bowl

Looking at the markets for a full two weeks prior to and including the Super Bowl, we see yet another story.

The three smallest markets leveraged 100+% RevPAR changes in the two weeks leading up to the Super Bowl, with Minneapolis/St. Paul again taking second after Indianapolis. As with Super Bowl weekend, New York and San Francisco/San Jose saw the lowest RevPAR growth in the lead-in to the Super Bowl, with growth under 35%.

Overall, a combination of low hotel supply and typically slow January and February performance resulted in extraordinary gains leading up to and during the Super Bowl for the Minneapolis/St. Paul area. This significant short-term boost was definitely a welcome change in the slow and chilly winter months, with the second-highest RevPAR increase in the last eight years. We’re already wondering what next year’s Super Bowl will bring to hotels in Atlanta!

This article represents an interpretation of data collected by STR, parent company of HNN. Please feel free to comment or contact an editor with any questions or concerns.