The past year has been characterized by recovery and transition, as the hospitality industry’s view shifted from the COVID-19 pandemic and toward mounting global economic turmoil.

Those massive strides made in 2022 and new challenges looming in 2023 have led to similar shifts in how industry analysts are approaching forecasting in the new year.

For most of the world, COVID-19 restrictions have largely, if not entirely, ended, and nearly all countries excluding China have welcomed back international inbound travel. Hotel demand has consequently surged globally as both domestic and international leisure, business transient and group travel started to rebuild.

The pace of recovery varies significantly by region — the U.S. and Europe reopened and ended restrictions earlier, while many Asia-Pacific countries only fully allowed travel as of the third quarter of 2022 — but global hotel demand is expected to be at or over pre-pandemic levels by year-end 2023.

With demand swiftly normalizing and the pre-pandemic period five years in the past, forecasters have started to look beyond the 2019 index when projecting future performance trends.

Rates Resetting

Over the past few years, the 2019 index has served as an important reference point for how hotel occupancy “should” look. However, with record-breaking rates and continued calendar shifts, finding a useful comparison has become increasingly difficult.

Poor performance over the COVID era led to massive growth in year-over-year demand, which in turn stimulated average daily rate growth. Hotel rates across the West faced further external pressure from well-above-average inflation, and as a result, ADR recovered much faster than demand coming out of the pandemic. While the index was initially incorporated into analysis and forecasting to provide context that year-over-year variance could not, the tables have flipped for ADR.

Hotels in Budapest, for example, are expected to end 2022 with rates 38% over the pre-pandemic level. While rates in Hungary’s capital will decline over the next 12 months, the decline will be modest, and ADR will remain on average 30% ahead of 2019. Year-over-year variance — which, excepting events and event offsets, remains in single-digit territory — will better help hoteliers understand performance dynamics, including the impact of the upcoming recession in 2023.

ADR may decline year over year due to new supply or an industry slowdown, as in Budapest, but today’s higher rates are largely expected to be sticky. The further ahead of the pre-pandemic level that rates run, the less useful the index becomes.

Calendar Considerations

While demand has been slower than ADR to recovery, shifting holidays and events increasingly impact the 2019 index regardless of a market’s recovery level. In the U.S., calendar shifts have consistently influenced indexes through the second half of 2022. Both Labor Day and Halloween shifted forward one week between 2019 and 2022, impacting the monthly demand index for August, September and October. In the U.K., two one-time bank holidays — the Platinum Jubilee Bank Holiday in June and the Queen’s Funeral Bank Holiday in September — affected indexes for those months.

To combat this, year-over-year comparisons are increasingly used in forecasting demand. While the 2019 index is still a consideration, especially in markets where demand hasn’t reached pre-pandemic levels, shifting views to consider traditional year-over-year changes allows forecasters to incorporate longer-term changes in post-COVID performance trends that might lead to aberrations in the 2019 index.

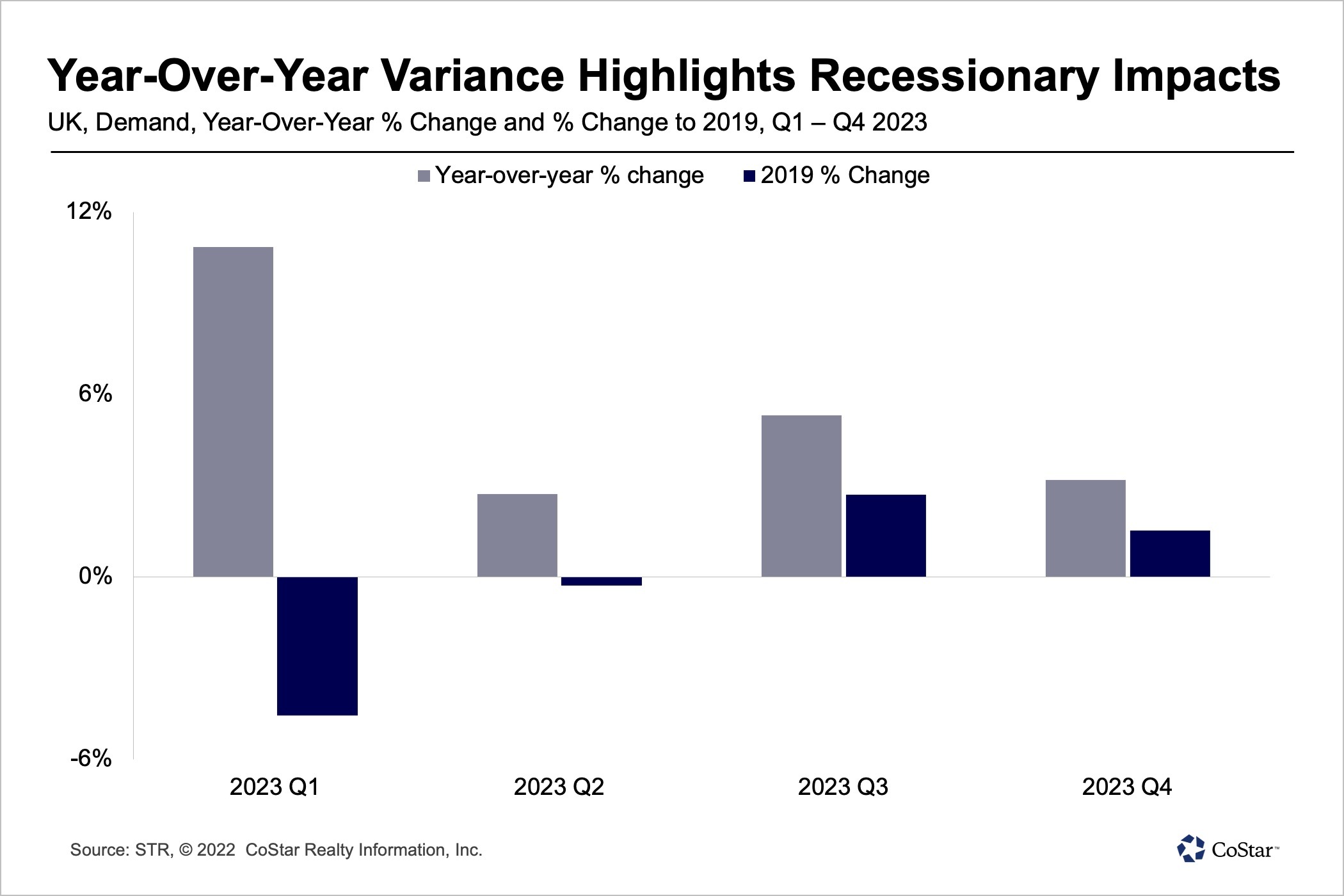

It also provides increased granularity in analyzing and forecasting performance in the context of the U.S. and European recessions expected in 2023, as modest adjustments to year-over-year demand growth can emphasize recessionary impacts.

The U.K. hotel demand index, for example, is expected to continue improving from the first through third quarters of 2023. Year over year, however, the second quarter of the year is the weakest, with demand only expected to rise 2.7% from 2022 as the recession impacts hotel demand.

Conclusion

Continued improvement in demand means that for many markets, year-over-year comparisons will once again become standard in 2023. The first quarter of the year, with comparisons to lower demand in early 2022 due to a surge in cases of the COVID-19 omicron variant, will likely be the last time the index will take center stage. The index is likely to remain one of many tools in the forecaster’s toolbox, but its importance will substantially decline over the course of 2023.

Kelsey Fenerty is a senior analyst at STR, CoStar's hospitality analytics firm.